Diary of a Money Manager, ep. 20

Noone's Ark

04.28.2024

Last week we learned that the US economy is barely growing—despite the federal government borrowing trillions of dollars per year and American consumers trillions more. In other words, the dreaded stagflationary “environment” which has appeared inevitable to some of us, myself included, now appears undeniable. But the stock market went up anyway (because lots of people are experimenting with AI on Microsoft’s and Google’s clouds) and the dollar remains historically strong (because rates are up and the world is scary and so on). Meanwhile, enraged though remarkably uneducated college students and their “allies” have taken over the common areas of a number of universities while their foil, Donald Trump, enjoys a bounce in the polls.

Speaking of foils, I used to regularly bash Ark Invest founder Cathie Wood— when her flagship innovation fund, aka ARKK, traded in the three figures(!) While I found her charming in person, in persona she’s sleazy and misleading and sanctimonious and entirely disingenuous—or else willfully ignorant. In other words, typical of her profession, which loves to spin stories into gold—for the fees. Wood encapsulates one of the two doomed stock market camps, the one that preaches that it’s all about buying the right things, price be damned. As a result her investors have endured a terrible couple of years, and she has made it worse by doubling and tripling and quintupling down on her already crazy price targets, which would be kind of a neat Jedi mind trick if markets worked that way but the Force is no longer with her.

Fast forward to a few days ago, when a shocked partner shared a Wall Street Journal article titled, Cathie Wood’s Popular ARK Funds Are Sinking Fast. A longtime reader, he was not surprised by Wood’s comeuppance—I’ve given him years to brace himself— but rather the scale of her wealth destruction. So I reminded him that, as Ben Graham observed, investment formulas (or theses or hypothese if you prefer) collapse at the moment of peak adoption, and at peak adoption there is peak price, because it's the popularity moving the price and not much else if anything, though maybe price targets help? Peak adoption at peak price is what’s known colloquially as a double whammy. Per The Journal:

By the end of last year, ARK funds had destroyed more wealth than any other asset manager over the previous decade, losing investors a collective $14.3 billion, according to Morningstar. ARK’s biggest inflows came in the months surrounding the innovation fund’s February 2021 peak, unfortunate timing for many investors.

But even those who got in on Wood’s ground floor have not done well. Since its inception nine years ago, Ark’s flagship innovation fund has returned 8.5% annually, well below the S&P 500 historical average of 9.9%. As Andrew Carnegie observed over a century ago, pioneering don’t pay, so no big surprise that someone who blindly bets on “innovation” would crash and burn, history be damned. But here was a bit surprised, at least by how Wood chose to mark her downfall—by going on a World Tour, first stop Europe. Here’s some snippets from an FT article published around the same time. It’s entitled, Cathie Wood takes her Ark ETFs to Europe as US investors jump ship:

Cathie Wood’s Ark Investment Management is launching its first three active exchange traded funds in Europe, courting a new continent of investors after a run of poor performance and outflows in the US.

Wood, Ark’s founder and chief executive, cited years of interest from potential investors across the Atlantic Ocean as she seeks to make her mark in the $2tn European ETF market. “Over the past decade, a substantial portion of our website traffic, subscriber base, inbound requests, and social media traffic have come from people in Europe — a clear signal of the strong interest and demand for Ark’s investment strategies within the European market,” Wood said in a statement.

Because if anyone knows how to read “clear signals” it’s Ms. Wood, I guess. Moving on…

Last week I completed my semi-annual foraging of the New York Stock Exchange, which yielded just twenty-six investable stocks; the eleven newbies are listed below. Id est, fewer than one percent of the listings on the world’s most prestigious stock exchange may be considered actual investments as opposed to speculations. One major reason is that the NYSE is littered with great ideas that never got around to making money. This includes many components of Wood’s various funds. Another reason for the slim pickings is that I don’t consider several large sectors, namely utilities, financial institutions, airlines and oil companies.

To explain why—or really why not—I might offer an exhaustive explanation full of insights and industry jargon. But this would be ironic and even hypocritical since such explications are the industry’s modus operandi, and that “look how smart I am, peasant!” schtick is one of the reasons that I refuse to invest in financial companies. So rather than pontificate, behold simple data in graphical form. Why explain why something should not work hypothetically when decades of history has taught you that it does not work? Because you may end up overthinking the obvious and be pulled into the dark side, like Ms. Wood’s customers for example. Why not expound theories of why something should work when you already know that it will? Because this is a waste of time that could be spent on more productive stuff, like foraging for cigar butts and wallflowers, for example. In the words of the late Charlie Munger: anything worth doing is still not worth doing well. Colloquially, time is money.

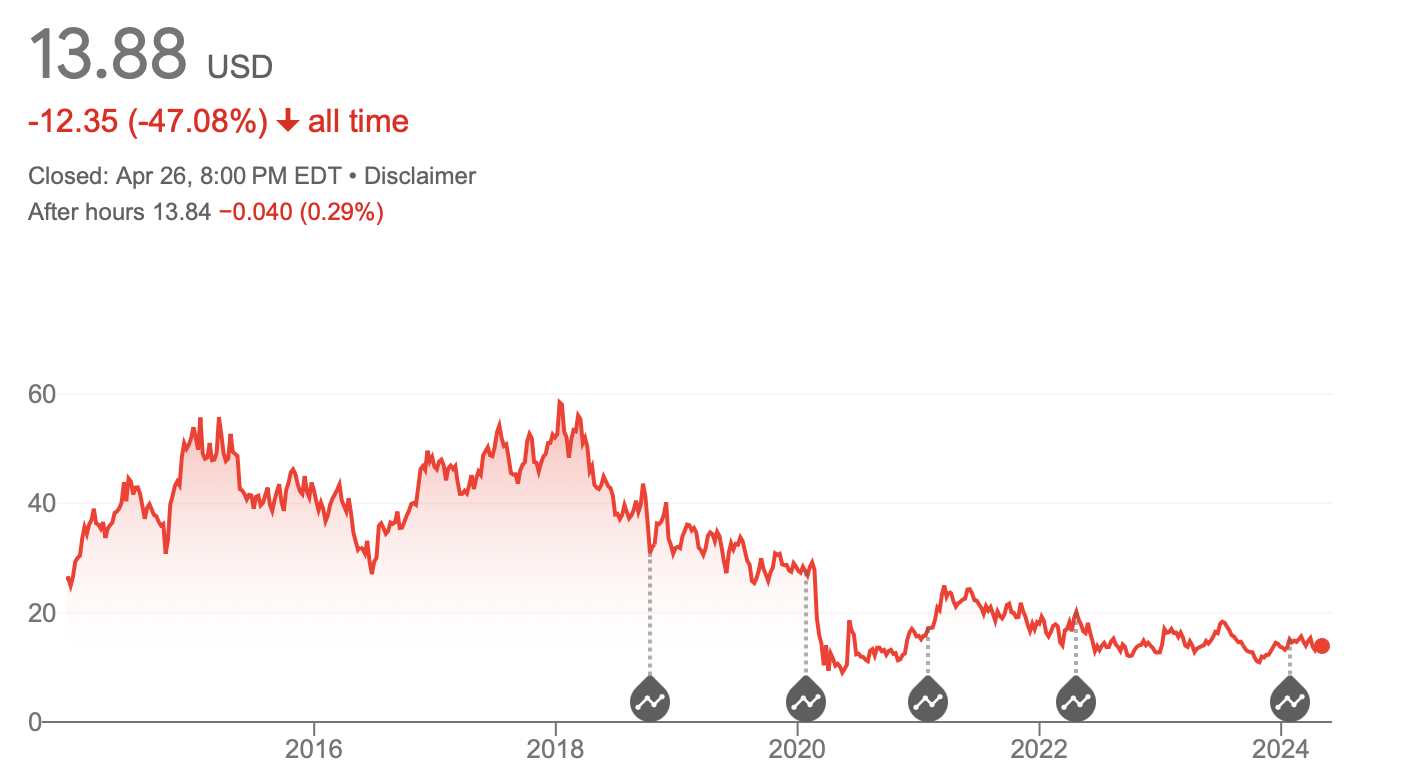

A caveat: I’ll ignore utilities entirely because they’re all burning huge amounts of cash and a few have declared bankrutpcy in recent years, which has the effect of destroying continuity. So first off, here’s the stock price of the country’s largest airline, American, since its latest reboot about ten years ago::

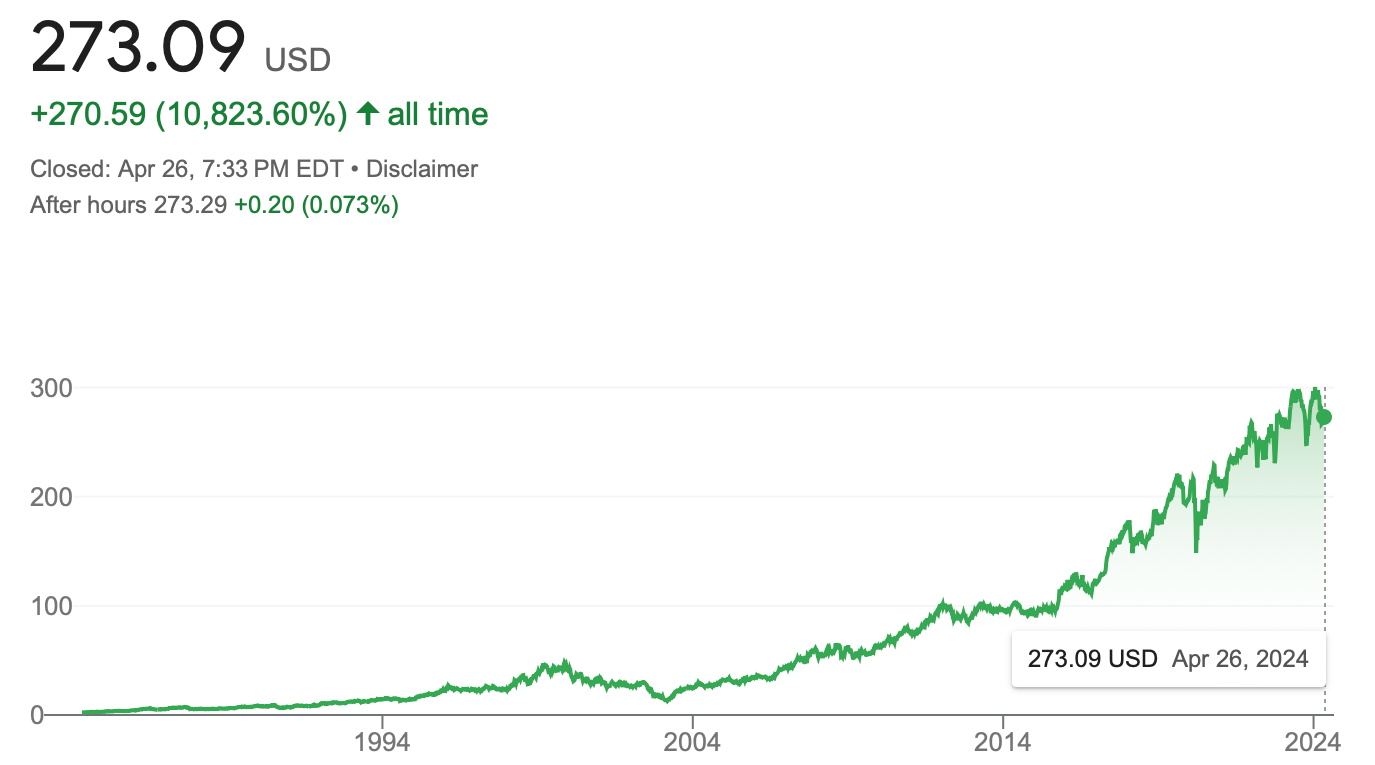

Now behold shares of the country’s largest oil company, Exxon Mobil, also since inception:

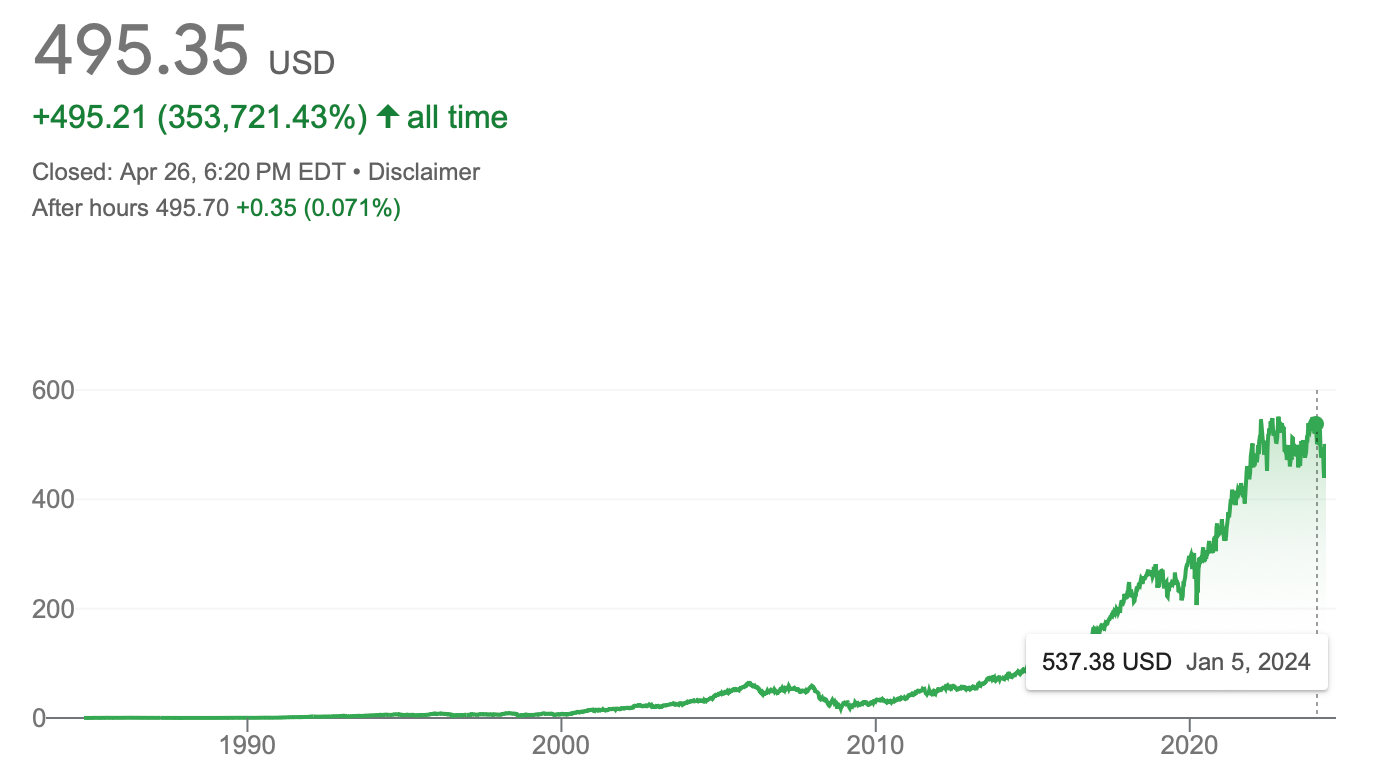

Lastly, here’s the nation’s largest bank, JP Morgan Chase & Co., which is also widely considered to be the best-managed:

Net-net: the country’s largest airline has managed to lose nearly half of its investors’ money over the past decade or so while the country’s largest oil company has made 8% annualized (exclusive of dividends) over the past forty years. And the nation’s largest bank has returned 7.5% per year over the same time period (also exclusive of dividends).

Only one of these stocks, Exxon, might have beaten the S&P 500’s historical annual return over time but a definitive answer would require a complex accounting of its dividend through the years. Suffice it to say that the two are close and that JP Morgan did a little less well. Which may seem like a wash, until you consider what a percentage or half a percentage a year can do over decades. (Here’s a tool if you want to see for yourself.) And to be honest, what are the chances that, four decades ago, an investor would have been so prescient as to pick what was to become the most valuable company in its industry? More likely that a lesser company would have been chosen, or else a basket of companies that would have performed far less well than the leader. A final note: What are the odds that one would have invested in the oil industry in 1984, just as it was coming out of an historic crash and was priced accordingly? In commodities as in real estate, timing matters a lot. In our example, Exxon’s investors got very lucky.

By contrast, here’s the performance of the country’s largest retailer, Wal-Mart, which comes out to nearly 14% annualized, before dividends:

Here’s the country’s largest homebuilder, D.R. Horton, which has achieved average annual returns of 15.5% over more than three decades.

Hungry for more? How about the world’s largest restaurateur, McDonald’s, which clocks in at 12.5%:

And the world’s largest athleticwear company, Nike, which has achieved an Olympian 17.5%:

Then we have the world’s largest consumer electronics company, Apple, whose historic annual return falls just under 20%:

Also, the world’s largest home-improvement company, Home Depot, at about 20% over the same time period:

And the country’s largest healthcare company, UnitedHealth Group, at 23%(!):

Finally, here’s Cisco Systems, a longtime technology “blue chip” that also happens to be the only pure tech stock in The Fund. Since inception 34 years ago, CSCO has yielded 21% annually. Bazinga!

You will observe that Cisco offers another, and far more important, lesson: Don’t buy on momentum but on price. But I digress. The point of all of these charts is that, over time, the inherent dangers of each industry have been “baked in” to the market values of even their biggest and most important companies. And because of that, and for whatever reason, their performance has largely fallen far short of the 21% historical return of Ben Graham’s almost all of the time. Still, some industries are clearly better than others, and tech is not necessarily the best bet. Surprise!

In order to beat the market’s performance with little risk, which is our aim, one cannot simply pick industries or stocks or—perish the thought!—ideas. Nor can one buy and hold or buy the dip without careful analysis. Instead, one must apply intelligence to all investment decisions, all the time.

Editor’s Note: Slow Money returns next week, with all of the numbers and portfolio data. Paid subscription required.

Marine Products Corp (MPX)

Fiberglass boats.

Earnings Yield: 9.4%

Dividend Yield: 4.87%

Medifast Inc (MED)

Weight loss supplements.

Earnings Yield: 35.3%

Dividend Yield: -

Meritage Homes Corp (MTH)

Arizona-based homebuilder.

Earnings Yield: 13.0%

Dividend Yield: 1.77%

Nucor Corp (NUE)

American steel.

Earnings Yield: 13.3%

Dividend Yield: 1.23%

Polaris Inc (PII)

Recreational toys.

Earnings Yield: 10.5%

Dividend Yield: 3.15%

Sealed Air Corp (SEE)

Packaging products.

Earnings Yield: 9.3%

Dividend Yield: 2.52%

Signet Jewelers Ltd (SIG)

Large multi-brand jeweler.

Earnings Yield: 10.6%

Dividend Yield: 1.14%

Tenaris S.A. ADR (TS)

Luxembourg steel.

Earnings Yield: 12.4%

Dividend Yield: 3.12%

Terex Corp (TEX)

Materials processing machinery and aerial work platforms.

Earnings Yield: 8.4%

Dividend Yield: 1.14%

Travel + Leisure Co (TNL)

Vacations.

Earnings Yield: 9.5%

Dividend Yield: 4.37%

Vector Group Ltd (VGR)

Cigarettes.

Earnings Yield: 11.6%

Dividend Yield: 7.79%