Subscribers,

You know the one thing that we can all agree on these days? That Mao reboot Xi Jinping is single-handedly destroying China’s economy and setting the Middle Kingdom back at least half a century because, um, he yearns for the days of the cultural revolution that so terrorized his family when he was a child. But also fear China’s relentless march towards domination in technology—from manufacturing to communications to blockchain to A.I. to social media to 6G—that clearly and presently presents a clear and present danger to, say, freedom, world peace and universal harmony. Moving on…

Ben Graham knew that markets were as irrational as the people who composed them, i.e. that human narratives often trumped math and therefore some stocks might take years to realize their value vis-a-vis market prices. But in 1929, Graham stayed invested in a market that he knew was bubblicious. Even worse, just before the crash he turned down an offer to be the first partner of America’s richest man, Bernard Baruch, who was cashing out. Twenty years later, a tenet of Graham’s approach would be to stay clear of a market “trading at historic highs.”

Which is where we are now, by any measure, e.g. the Buffett Indicator, P/Es, price levels, leverage, etc.. Because of this, I’m (mostly) shutting down a few days earlier than our intended October vacay, October being the worst month for markets, historically speaking.

cigar butts & wallflowers

So how did we do in a year? Pretty damn well, as it turns out…

First, the cigar butts. These are the smaller and less important companies selling at 33%+ below their quantitative values. These are the stocks that fueled Warren Buffett’s original partnership and, in my opinion, the ones that smaller but enterprising investors should be most interested in—if they want to beat the market rather than follow it. The danger with CBs is that they tend to perform above average in up markets and below average in down ones, as the “flight to safety” impels retail investors to rush to the presumed sanctuary of large and important stocks when momentum reverses.

That being said, despite taking four weeks off to recalibrate—all weeks in which the benchmark S&P 500 went up, mind you—our Cigar Butts portfolio (1.0-2.0-3.0) advanced 52.6%(!) which is far more than the 28.6% gain in the S&P 500 and nearly three times the advance of Cathie Woods’ flagship ARK Innovation(!!) which is the most followed ETF of the year. (ARKK gained 18.1% over the same time period.) Net-net: rather than our goal of 5% alpha, we achieved 24% and 34.5% alpha versus the benchmark and ARKK, respectively(!!!)

Our wallflowers, designed to do well in advancing markets, bloomed early then began to wither as the Xi-as-Thanos narrative took hold, 22% of the WF 3.0 portfolio being in Chinese stocks. This eastward tilt was not intentional but a result of the domestic stock markets’ relative frothiness. Indeed, I was forced to limit the number of Chinese wallflowers out of an abundance of caution, which turned out to be somewhat prescient, because the Wallflowers Portfolio (1.0-2.0-3.0) advanced 52.6% since last October, exactly the same as our cigar butts. Yes, I have triple-checked the math and am somewhat weirded out by this. Also happy.

Altogether, Cigar Butts 1.0, 2.0 and 3.0 yielded +13.5%, +37.9% and -2.49%, respectively while Wallflowers 1.0, 2.0 and 3.0 yielded +13.1%, +38.5% and -2.59%, respectively. Two weeks were taken off between each iteration.

At closing time, i.e. this weekend, the Cigar Butt Portfolio 3.0 trades at 0.39 of its quantitative value, implying a roughly 150% gain in order to achieve price-value parity while the Wallflower Portfolio 3.0 now trades at 0.40 of its quantitative value, also implying a roughly 150% gain in order to achieve price-value parity. Id est, although the strategies differed, the two portfolios are quantitative twinsies in every way. Moving on…

lessons learned:

Ben Graham is smarter than me. (Enough said!)

It’s about the portfolio, not the stock. This seems to be the hardest lesson for readers to accept but it may be the most important. Our portfolios are quantitatively constructed per the mindset that if you protect your downside the upside will take care of itself, and so it has. The portfolios are not menus. I am not a stock picker. The end.

Preservation of capital need not come at the expense of returns. One of my favorite parts of The Intelligent Investor is Graham’s debunking of the conventional wisdom that reward is a function of risk. Instead, Graham proffers that the amount of work and intelligence one puts into investing—as well as the consistency and discipline with which both are applied, I might add—are what determine results. A little does not go a long way here. Hobbyists and day traders, beware.

Our third iteration were probably not diverse/big enough. On the other hand, that less than 2% of stocks I’ve analyzed recently may be considered investment-worthy is clearly a sign.

Be early. Had we not gotten into the market when we did, we’d now be desperate rather than sober.

Trendy stocks are more stressful than necessary. No need for momentum, memes, controversy and narratives—unless 53% year is not enough for you.

China

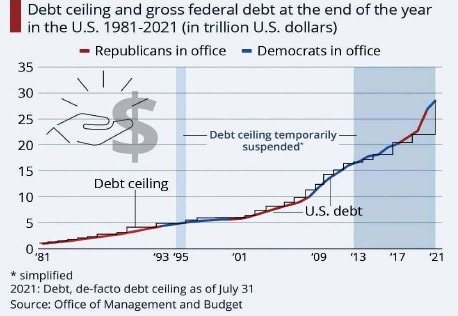

The anti-China narrative has not really picked up steam in the last several weeks but it hasn’t run out of it either! The New York Times has now christened China’s regulatory moves en toto, The Corporate Crusade, which is curious verbiage for an atheist country imho. That so many pundits are so bitterly attacking China and personally attacking Xi Jinping, and that China and Xi stoically ignore them, convinces me that China is winning the economic Cold War. (Caveat: I am no geopolitical expert!) Or maybe the daily attacks, increasingly personal, are to distract from America’s annus horribilis: Covid’s second coming, Afghanistan’s exit, the unfathomable growth in debt over two years, political gridlock despite a unified government, racial division, record inequity, the president’s mental acuity etc. You know it’s bad when mellow documentarian Ken Burns says we’ve reached a low as bad as before the Civil War(!) Then there’s the Federal Reserve’s tapering/tightening routine 2.0—a guessing game/bluff in equal parts theatrical and tired. Powell et al would like to remind us that things will go back to normal any day now, i.e. that trillion-dollar deficits, runaway inflation and underemployment are transitory, but we al know that the U.S. will not be taken off of the fiscal life support machine that began pumping in earnest a dozen ago, nor will the money pump be dialed down more than less than a notch. If you don’t believe me please read the absurdist and paywalled article in yesterday’s Bloomberg entitled, Tapering Doesn’t Mean Tightening for Central Bank Money Printers. More money, no problem!

But back to China, where a very large real estate developer called Evergrande is going bust, which absolutely must mean the end is near for our geopolitical nemesis! Or maybe China is shrewdly using Evergrande’s crisis as an opportunity to increase support for the non-financial, i.e. productive, sectors of its economy, mostly technology? We’ll see how it all shakes out. But there’s a lot of Americans, e.g. Howard Marks, Charlie Munger and Ray Dalio, putting their money on red these days.

Meanwhile, the powers that be here are addressing an admittedly economic war with military thinking, in other words there seems to be little appreciation of the difference between the economic vs. geographical. Ergo the recent deal to sell nuclear submarines to Australia that has pissed off France and pushed Europe closer to China. Worth noting that empires always collapse by spending too much money invading other countries that don’t want them there, but when you have a hammer everything is a nail and so on and so forth, and American exceptionalism may prove the exception that proves the rule. But the verbal warnings of a red menace, increasingly dire and histrionic, don’t seem to be landing, most likely because China has an indifferent retort, i.e. We are not an empire, only a country.

Any questions?

If you read The Wall Street Journal last week you’d have thought that the possible default of $88 billion in tacky Chinese condo junk bonds is the world’s biggest story—even, as they loved to say in 2008-9, an existential threat to the global financial system. Color me skeptical. The bigger story may be that China is doing what we couldn’t in 2009, i.e. allowing the markets deal with a market crisis. How, er, communist? I practically worship the Journal—at least the news part—but its editors are clinging to misguided prejudices that 1) China should be just like us; 2) We did everything right back in 2008-9; 3) regulation is inherently anticapitalist.

Much has been read into the financial troubles of Chinese real-estate developer Evergrande—whose last financial statements were signed off by an American firm, free and clear of any warnings btw—but also of the recent arrest of two HNA executives in Beijing last week, on corruption charges. Of course we know nothing of sleazy real-estate developers or corrupt bankers in America, or so you’d think reading the commentary. Meanwhile, the Elizabeth Holmes/Theranos trial is framed as personal drama, like the new Kristin Stewart/Diana Spencer biopic, NOT the grand reveal of public-private corruption in the United States of America. As Graham observed, we cling to our prejudices above all else. And as Kurt Vonnegut used to say, and so it goes…

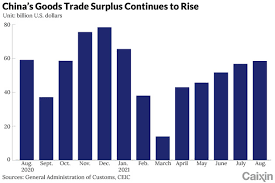

Late on Friday, the greatest Sino-American diplomatic crisis of our decade, the extradition battle involving Huawei’s CFO and two Canadians, was resolved with no shots fired and no deaths. Which makes it different than when we bombed the Chinese embassy in Belgrade, so maybe things are actually getting better? Who knows! Here’s a chart:

Finally, I’ve read that the U.S. Commerce Secretary is putting together a group to travel to Beijing soon, in order to “hunt” (the secretary’s words, not mine) for new business opportunities there as Nike’s sales in China have plateaued (see above); crypto has been outlawed and Alibaba (BABA) has been asked/told to sell a small stake in a local television station.

inflation

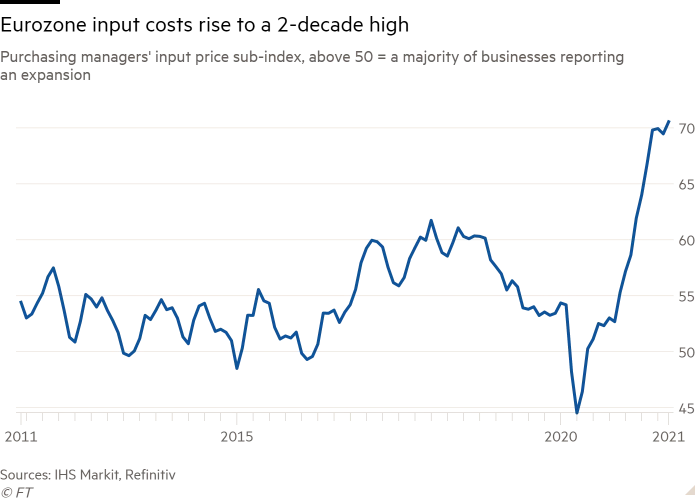

Outside of China, there are now gas lines in the UK and Europeans are beginning to freak out about the massive spike in the cost of fuel just before fall/winter. What we used to call the real economy is biting back. Elon Musk has not offered up a technological hack as of this writing...

market diary

The major indexes were ultimately mixed last week. The DJIA and S&P 500 advanced by 0.6% and 0.5%, respectively, while the Nasdaq Composite was flat.

On the New York Stock Exchange, 1721 of 3568—i.e. 48.2%--stocks advanced last week. The NASDAQ saw 2266 of its 4922 traded issues—i.e. 46.0%--gain value.

ARK Innovation ETF (ARKK), our volatile proxy for popular momentum stocks, aka speculations, fell 3.6% last week(!) We are less than a week from the fourth quarter and, year-to-date, ARKK has declined 5.9%(!!)

sentiment

As of this weekend, both the DJIA and S&P 500 indexes trade at a 32% premium to quantitative value (QV); the NASDAQ Composite at a 44% premium; and the Russell 2000 +101%(!) Historic trading ranges are estimated as follows:

DJIA: 17696 (low) to 39619 (high)

S&P 500: 2265 (low) to 5072 (high)

NASDAQ Comp: 7020 (low) to 15717 (high)

Russell 2000: 750 (low) to 1680 (high)

Zoomie

There will be class/AMA tonight! Invitations to follow…

Fund Stuff

Graham disciple and Pacific Partners founder Rick Guerin made only one major mistake in his career, which was using leverage, which Graham explicitly forbids. Like Graham’s exposure to the market in 1929, Guerin’s transgression was nearly fatal. Both men’s investors “lost” about 70% of their money in their respective crises, more than four decades apart, but most of them hung on and were not only made whole but made very rich as a result of their loyalty. Still, I imagine these made for some very unpleasant years for everyone involved. Fund 1.0 is playing by the rules, which for now means being patient.

So I’m looking for something to do until market conditions are conducive to actual investing again. My strengths are independent analysis, ability to complete sentences and form paragraphs, love of work, and extreme spelling proficiency. My major weaknesses are in the areas of team playing. Also I swear a lot, I speak only one language and credit card companies hate me.

random observations/conclusions

In case you were wondering, and much like Celine Dion’s heart, the boring kitties will go on—for now. Because Asian stocks are not at historic highs, and our BKs happen to be very Asian.

Lastly, the North American box office is off big time again this weekend from 2019. Receipts for Friday through Monday will be down 59% or so since the same weekend pre-pandemic*. Making things worse for Disney, the dominant film studio, is its weeks-old decision to release new films only in theaters, a decision made as sign-ups to its Disney-plus streaming services slowed to a trickle. There are few good choices left these days. Or maybe that’s just showbiz.

James

* Shang Chi, Disney-Marvel’s China movie, remains #1 in its third weekend and will be the most successful American film this year. So hmmmm.

weekend read:

charts:

more data & analysis at jamesdscurlock.com