Real Money, vol. 12

Real Money, vol. 12

My October Symphony

Subscribers,

What a week.

The news, by which I mean the running commentary that tends to run farther and farther from the underlying facts until they’ve been forgotten or discarded as no longer relevant, was dominated by some Congressional melodrama involving a bunch of very old people staring down a bunch of much younger (not to mention angry!) people over trillions of dollars that don’t yet exist. Guess who thinks they won? Not the old folks and maybe the younger ones but definitely the stock market, which marched forward despite so many signals to retreat, including the rather embarrassing display of political gridlock in a country run by a single party(!) This presumably because investors only care about the Federal Reserve, which can print as much money as it wants to, and behind closed doors, thank you so much, no brinksmanship or even debate necessary…

Speaking of the Fed, it turns out that no less than its Vice Chair has been day trading into the Fed’s market purchases of stocks and bonds. Which is not a good look, not at all! Said Vice Chair claims it was all planned way in advance and so on and so forth, nothing to see here, boy is that China corrupt! Moving on…

This is the first of five Real Money issues sans numbers, i.e. stress-free! The original plan was to take the month off completely, October being infamous as the month of Black Monday, Black Tuesday, Black Thursday and the Bolshevik Revolution (not that I’m superstitious, mind you!) but let’s see if it works as a period of reflection, of seeing the forest for the trees, so to speak.

First some trees: As I write, the world’s #1 smartphone, app and movie are all Chinese; the best-selling band is Korean. Last week, the (American) Tony Awards hit an all-time low in ratings while Disney’s Broadway hit Aladdin managed exactly one reopening performance before Covid shut it down again. How Broadway can survive with Covid and without foreign tourists is beyond me, though I’m not that imaginative. How Hollywood can dominate in the streaming age, well, those days are probably gone too.

There was some good news last week, or rather good news/bad news. On Friday, both Australia and Vietnam spontaneously reopened after months of severe lockdowns. Which means that now only China, Taiwan and Singapore seem to be sticking to a zero-tolerance approach to Covid-19. Elsewhere, reopening has not gone as planned. The Western Hemisphere is staring down fuel shortages, sustained inflation and joblessness, shrunken GDPs, broken supply chains and a nearly broken (and confused) populace.

Behold the new normal:

Energy is expensive! Record coal and LNG prices are causing all kinds of anxiety and disruptions, including rolling blackouts in parts of China that may impact factory activity and therefore the availability of many, if not most, consumer products. (Note: iPhones are made of coal! Who knew?)

There are 1970s-style gas lines in the UK and, far scarier, no consensus as to why there are 1970s-style gas lines in 2021. The British Army is now involved, driving trucks, er, lorries. Maybe they’ll call back Prince Harry? Stranger things have happened! Keep calm and all that.

Actually, there are lines everywhere. Hundreds of thousands of containers are loitering off the coast of Los Angeles, for example, not only because of a shortage of drivers and Covid protocols but because American ports do not open 24/7, unlike in other countries (ahem).

No one wants to be around strangers, if it can be avoided. Demand for private jet travel is so strong that Berkshire Hathaway’s NetJets, the world’s second largest air carrier by number of planes, has stopped selling new jet cards. Also, AirBnB now has more listings than there are hotel rooms—in the world.

Restaurants, at least the ones that survived the first and second waves of Covid, are getting strangled by higher prices for labor, food and, as stated before, energy. It’s so bad that the National Restaurant Association is begging for another bailout, a la PPP.

The debt ceiling will be breached before the end of this month—or else it will be eliminated, which both Janet Yellen and Warren Buffett would like to see happen. Nobody knows! Either way, won’t the flames of inflation be fanned all the more? one wonders, before acknowledging that these days, one must choose one’s fires, figuratively and literally. Economists are curiously silent though Fed chairman Jerome Powell recently confirmed that he was wrong about inflation being just a blip.

The new economy came back first but the old economy is coming back harder, would not be a bad reopening theme. In my opinion!

But we still find comfort in the little things! While the President of the United States couldn’t get stimulus through Congress, last week the governor of California did sign legislation, dubbed the FreeBritney bill, to protect certifiably crazy former child stars from their parents.

Asia is #winning. Last week the hotly-anticipated and much-delayed James Bond film premiered to fabulous reviews, only to be upstaged immediately by a Korean mini-series, The Squid Game, which is already Netflix’s biggest show of all time and is so popular that, per FT, “South Korean internet service provide SK Broadband has sued Netflix to pay for costs from increased network traffic and maintenance work because of a surge of viewers.” Can Bond do that? No, no he cannot.

But the above are all data points available from other sources that reflect nothing more than transitory and mildly entertaining trends, as far as we know. What matters a great deal more to investors is 1) whether the markets are about to crash; or 2) whether it’s safe to buy stocks at the moment.

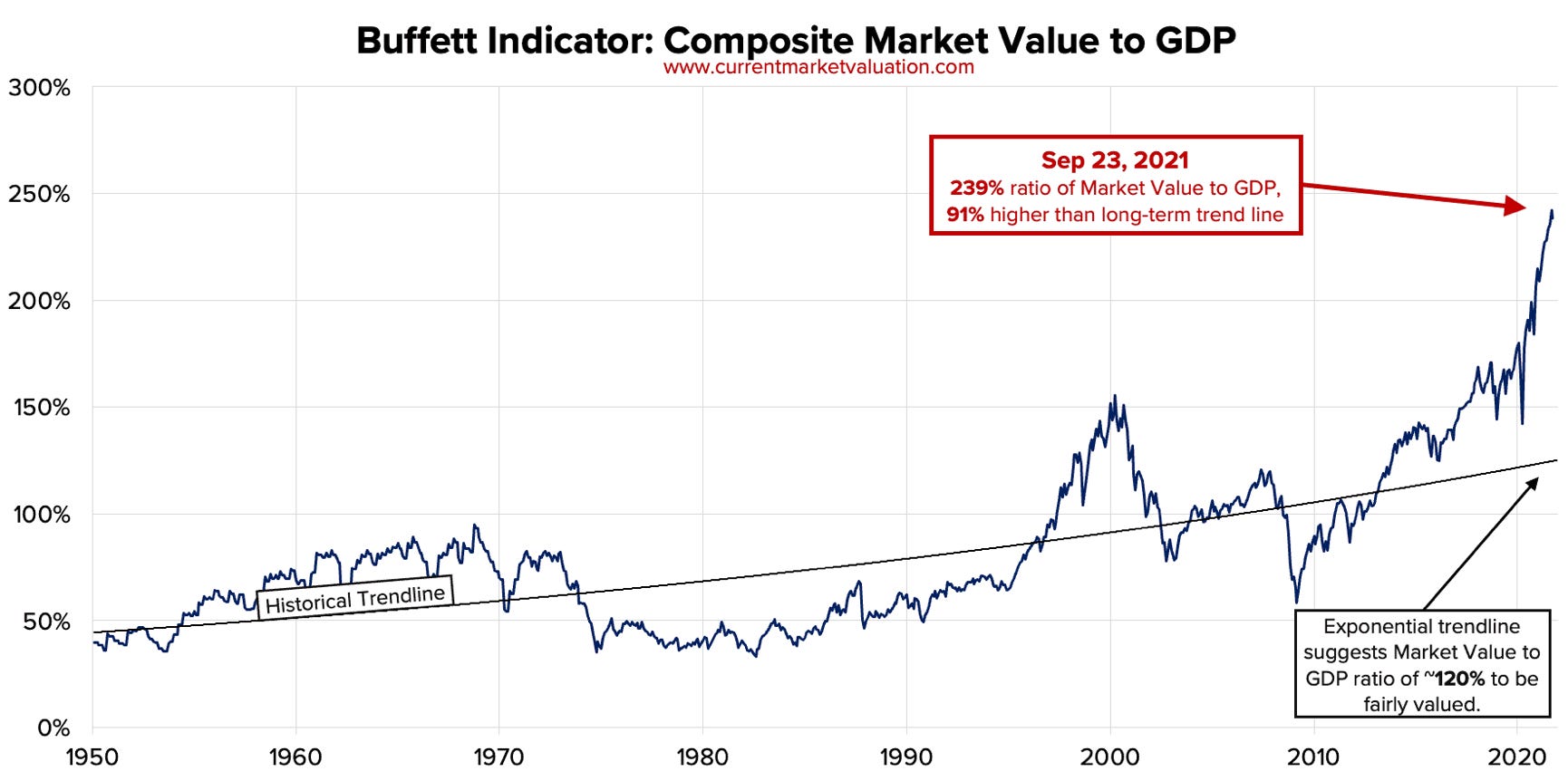

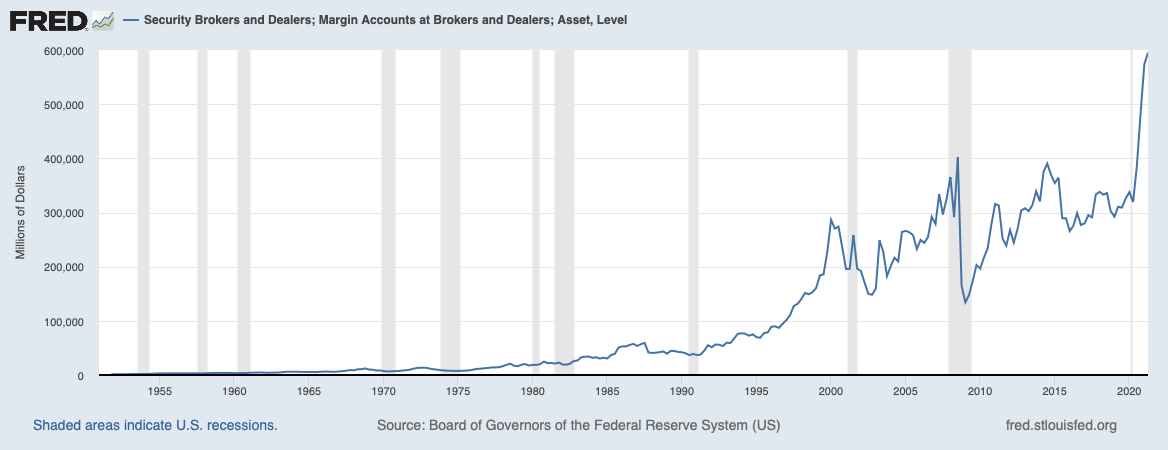

The answers are 1) probably; and 2) no. At the moment, the price-earnings (P/E) ratios of the Russell 2000, S&P 500 and NASDAQ Composite indexes are 366, 30 and 34, respectively versus a historical average of 12-15 (per WSJ). The Buffett Indicator, which measures the value of the US stock markets against the domestic economy, is at 239%, which is 91% higher than the historical average. Our valuation measures, aka QVs, show the major indexes to be over-valued by just 33-100+%(!!) Other bubblicious indicators, most notably a dramatic rise in IPOs and margin debt within the last several years, abound.

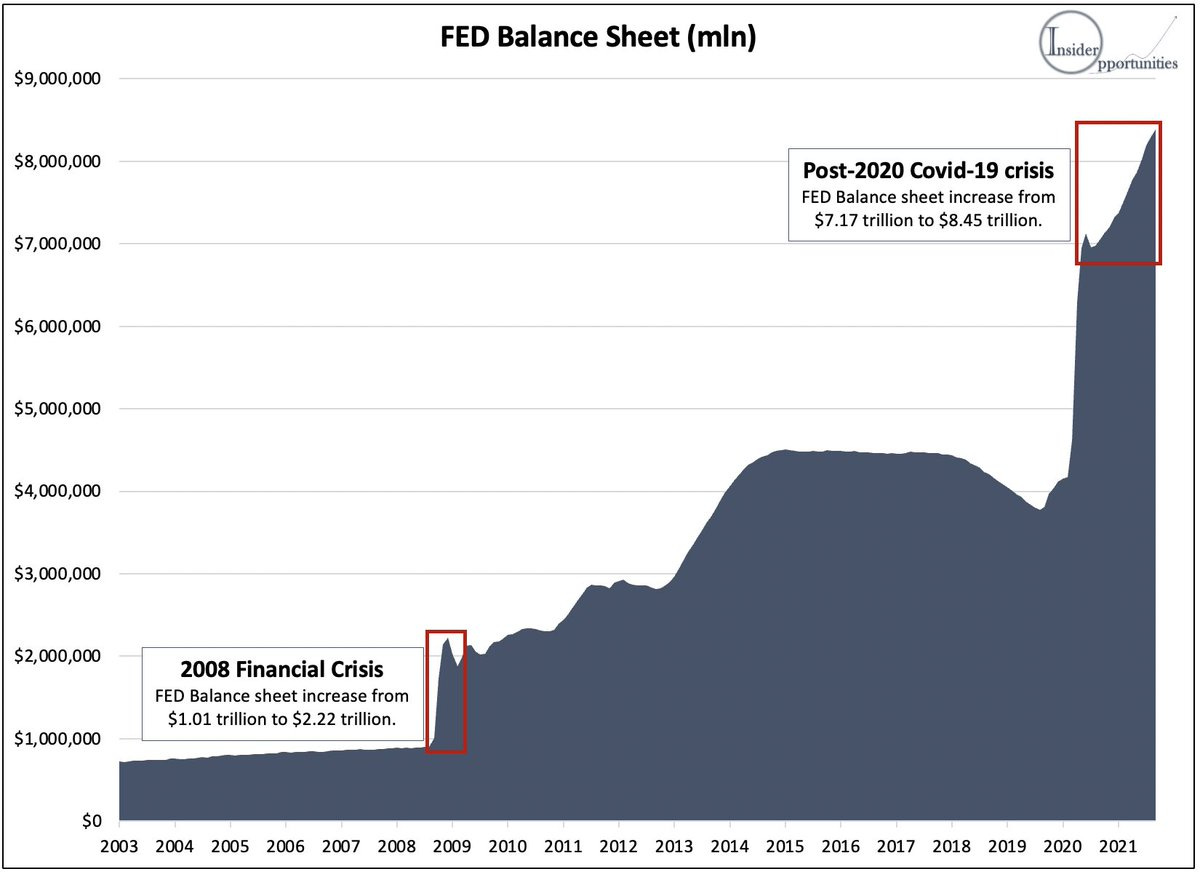

Here’s how it looks in graphic form:

In other words, caveat emptor! but also a few caveats:

There are large and important companies selling for substantial discounts to value that could be considered investment-worthy. However, they are all Chinese red chips, i.e. China-based companies trading in New York or Hong Kong (or both). We’ll call them chrysanthemums; portfolio to come in November.

After a long absence, volatility has made quite a comeback in the last couple of weeks. Keeping in mind that the initial—and very sharp—stock crash/recovery was provoked by pandemic panic/Fed action, it is very possible that a corollary may be provoked by the Fed, creating an investment-worthy market in a matter of weeks, maybe even days.

For the first time in history, there are two economic super-powers whose fates are inextricably linked but whose stock markets have been divergent for some time now. This creates opportunities that Ben Graham might not have foreseen, and which he did not foreclose.

More on all three of these points next week.

James

p.s.: no class this month…

p.p.s.: our surviving portfolio, the boring kitties, aka i/bets, will be back in November with cumulative results published from our last update.

weekend read:

weekend chart:

more data & analysis at www.jamesdscurlock.com