Slow Money, vol. 64

Slow Money, vol. 64

fortune favors the old

Subscriber,

As you may have heard, last week a supermajority of Tesla shareholders voted to hand over about 10% of their collective ownership in the company to its CEO, one Elon Musk. Even if Musk were not running several other companies, including another AI-centric one, this event would be unprecedented. But it may form a precedent, like when Michael Eisner got the first nine-figure executive payout as CEO of Disney decades ago. And/or Musk’s gambit may herald a new kind of greenmail, which is sent from within the C-suite. With executive pay growing faster than any time in at least the last fourteen years, as noted tody by the FT, this seems a curious time for executives to feel underpaid. In any event, a rubicon has been crossed and we’ll see what’s on the other side.

Which begs a question—not whether the market is efficient, of course it isn’t, but whether it’s rational. In Tesla’s vote we have the spectacle of shareholders voting in the CEO’s interest, either out of “fairness” (the company’s argument) or else out of a theory that doing so will inure to their benefit at some point in the future, persumaby when Tesla has a promised gigafleet of AI-driven taxis and semis and so on and so forth. Anyway, Musk’s compensation machination is either 4D chess or extortion, that’s in the eye of the beholder, but voting to give a single executive $50 billion that the company does not actually have in order to keep them more focused on one particular endeavor versus many others just seems, well, unprecedented and possibly disruptive, the latter being Musk’s specialty of course. As a Tesla shareholder, which I am not, one must really believe that not only is Musk the smartest man in the world but that he is the best executive in the world and also that his full loyalty can only be triggered only when he is in full self-driven mode, i.e. when he is getting a larger share of the equity, not to mention the votes. It seems to me that one must also believe that Tesla is the most valuable company in now and forevermore and maybe even that capital is not fungible. Calculatee the probability of each of these things being true, multiply them, et voila! You now know the odds that Tesla is a great investment at the moment.

I don’t love the odds, but at least Tesla is not in the digital ads business, previously described here as bubblicious. Now The Wall Street Journal finally has done the math in a weekend article titled, Amazon Has Upended the Streaming Ad Market, and Netflix Is Paying the Price. For those of you who did not go to business school in the early 1990s, Amazon is what is known as a bad competitor, mostly because they value market share over profits. Per The Journal:

The streaming ad market was upended earlier this year when Amazon converted its entire Prime Video subscriber base to a new ad-supported version, giving customers a chance to switch back to ad-free streaming for an extra $2.99 a month.

Prime Video’s large ad-supported subscriber base means it has a significant amount of ad inventory that is affecting the negotiations that Netflix, YouTube, TV networks and other streamers are having with advertisers as they commit to buying billions of dollars in commercial time for the coming TV season—a process known as the “upfronts.”

The e-commerce company is driving down ad prices for everyone, analysts and ad buyers said.

So it sounds like Netflix is not the only victim here. Also, although ads are assumedly about to get far more creepy personalized thanks to AI, there must be an upper limit to the amount of advertising that can be sold in a world whose leading economy is growing at 1.3% per year, and that upper limit has probably been reached by now. The question is to what extent digital ads are considered commodities, which would determine the direction of their prices, and I don’t know the answer to that, though if I were selling something I would be more likely to advertise it on the platform where it might be purchased in real time rather than during some tv show where the viewer would have to recall it after hours of binge watching plus maybe another eight hours of sleep. So we’ll see how this all shakes out and shakes up but if I were invested in an ad-dependent business such as Netflix, Google, Meta, Amazon, Disney, Paramount, etc., etc., I might be re-checking my assumptions about now.

Speaking of assumptions, most of my time this year has been spent shoveling a massive slush pile of zombie crap, which is probably the only sense in which I resemble a private equity manager. I have begun to imagine myself the stoic dealer at a cold table in a Vegas casino, maybe after the Sphere releases thousands of drunk and excited people, some of whom will hit a jackpot by virtue of the sheer amount of money being tossed around, in which case there will be a lot of bells and whistles and cheers and forgetting how much money was put into the machine or into my pocket before said jackpot. Casinos are very efficient even though the dealers are the only rational players.

It is a boring lot in life to play by the odds over and over again and I assume that most people do it for the paycheck. So it was that a bunch of investment advisors have reportedly been fired by Wells Fargo for using devices that made it appear that they were working when they were not, via an Amazon.com-purchased device that jiggles your mouse or whatever. But there is probably not that much for them to do at the moment anyway, except maybe read articles about how they are being replaced by AI. My advice for them is to manage their expectations better. For example, I considered myself extremely busy last week for foraging three investables, two of which have appeared on these pages at least once before (see below). Also I learned that we are in an increasingly efficient irrational market.

I consider learning the most valuable work, and I think that context is important. Here’s some:

Investors and traders thrive on inefficient markets but only investors avoid irrational ones. So it was that Warren Buffett went on hiatus in 1969, because he considered the market to be an especially fraught casino, i.e. one where the dealers were behaving like their customers. Traders, on the other hand, often cannot tell the difference between inefficient and irrational markets, or else they don’t care, particularly when the market is going up and they are leveraged. Think of Melvyn Capital melting down during Memestock I, or Carl Icahn losing $9 billion shorting the S&P 500 last year. (These examples are distinct from the famed collapse of Long Term Capital Management in 1998, which was ultimately the result of a black swan event—i.e. Russia’s default—plus overleverage, though in retrospect it was irrational for investors to lend Russia so many dollars in the first place; then again, investors should know that you don’t have to originate the sin to suffer for it.)

My point is that the biggest threat to the investor right now is not that interest rates or inflation will not come down quickly enough, or that Europe will elect right-wing politicians, but that the market will lose its collective mind. Add the self-diluting Tesla vote to a pile of evidence suggesting that it has already, evidence that includes the resurgences of crypto, meme stocks, same-day options, single stock options and an AI delirium that has big tech investors partying like it’s 1999.

A counterpoint: during the four-plus years I’ve been doing this, the 52-week lows highs and lows have generally followed the broader market trend. In other words, if the market was moving up, there would be a lot more 52-week highs than lows, and vice-versa. Now it’s the opposite. The markets have been on a collective tear, yet The Wall Street Journal counts well more than twice as many stocks trading at annual lows than annual highs.

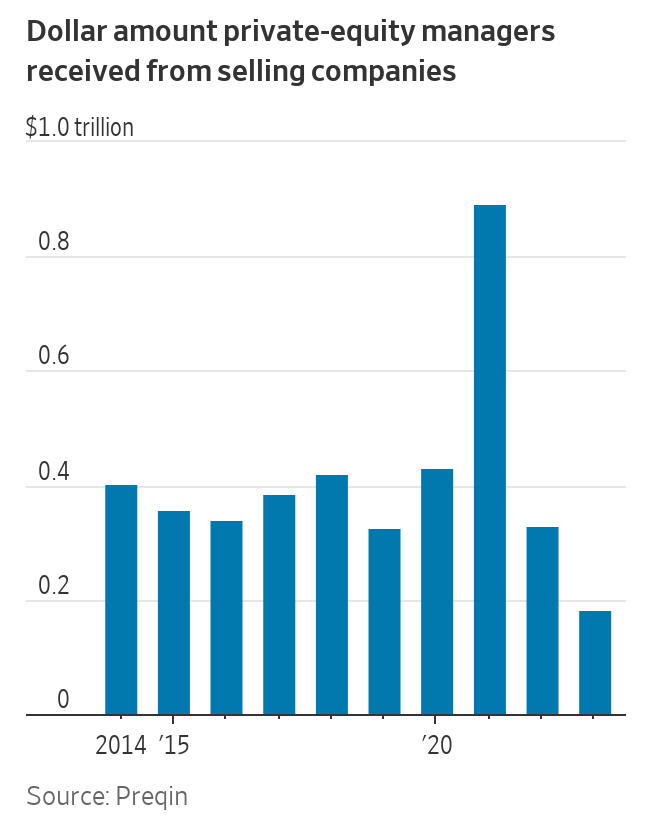

One more: I’ve long discussed here the catch-22 that private equity firms cannot exit many if not most of their holdings because they are probably worth less than their investors have been led to believe, which causes them to load up these investments with more debt, which makes them even less valuable. Even in a rising market, public investors simply aren’t buying the narratives that their private counterparts (which may include themselves) bought not so long ago. The result, as the Journal reported last week, is that a lot of assets are being sold in the private markets at a substantial discount. Here’s what this looks like in graphical form:

Which suggests that while the casino may be hopping, there are still cold tables to be found. In the land of the blind, the one-eyed man is king, and the public markets still have at least one eye open—for now.

James

52-Weeklings

Cigar butts and/or wallflowers among the 93 US-listed companies trading at 52-week lows this weekend:

Solventum Corp (SOLV)

Medical products and services company, spun off from 3M in 2024.

Earnings Yield: 14.7%

Dividend Yield: -

Winnebago Industries Inc (WGO)

Storied recreational vehicle manufacturer.

Earnings Yield: 12.8%

Dividend Yield: 2.25%

Investable(s) culled from NASDAQ’s short list of small cap value stocks:

Ingles Markets Inc (IMKTA)

Regional family-owned grocery store chain in the Southeastern US.

Earnings Yield: 17.2%

Dividend Yield: 0.97%

WARNING: GRAPHIC CONTENT!