Slow Money, vol. 72

Subscriber,

Last week’s headlines include the first interest rate cut* in years and a major escalation of hostilities in the Middle East. Meanwhile the stock market rotation continued. From Monday until Friday, the “small-cap” Russell 2000 gained 2.1% versus just 1.4% for the benchmark S&P 500, the latter now a proxy for the so-called Magnificent 7. Since late June, R2K is up 10.4% versus just 4.2% for SP500. Which seems significant.

Yet, for many, Bloomberg’s Friday afternoon headline said it all:

Fed’s Rate Cut Sends Already-Stretched Valuations Even Higher

The financial website noted that US stock valuations are already higher than the start of fourteen past easing cycles. Which explains the market’s vertigo when one might have expected euphoria. Moving on…

Let’s say you buy an asset for nearly two billion dollars, invest nearly a billion dollars more in said asset, then sell it for about half a billion dollars twelve years later. Would that be a good or bad outcome? I am speaking, of course, of Indian hotelier Oyo’s acquisition of storied budget lodging chain Motel 6 from private equity giant Blackstone, described thus by The Wall Street Journal yesterday:

The all-cash transaction with Blackstone ends an unusually long period of ownership by the private-equity firm, which acquired Motel 6 in 2012 in a deal valued at $1.9 billion. The pandemic delayed Blackstone’s exit from the investment, according to a person familiar with the matter.

Blackstone poured $900 million into improving the chain’s real estate and has spent the past dozen years selling off hundreds of individual Motel 6 properties, as it converted the chain to a franchise company, according to the person familiar with the matter. The investment firm has sold almost all of the more than 550 Motel 6 hotels it acquired 12 years ago.

“This transaction is a terrific outcome for investors,” said Rob Harper, head of Blackstone Real Estate Asset Management Americas. In all, Blackstone more than tripled its investors’ capital and generated over $1 billion in profit, he said.

So if your answer to the question was “terrific,” Blackstone says you win. Which was probably not the answer that came to mind! So what’s going on here and what does it mean, if anything?

Firstly, Blackstone’s Mr. Harper’s assertion that investor’s capital was tripled seems at once unlikely, vague and possibly irrelevant. Let’s say, in the best case scenario, his clients actually tripled their investment over twelve years. That’s a 9.6% annualized return, which would be worse than an S&P 500 index fund and far worse than the Graham method’s historical return of 21%. And this for an investment that was highly leveraged and concentrated in a single company operating within a highly competitive industry, i.e. this was a riskier proposition than investing in a liquid and diversified index fund or value portfolio. Then again, Blackstone had a trick up its sleeve: sell the real estate, keep the brand. This seems to have worked for Motel 6 where it has failed for others, e.g. Macy’s and Sears/K-Mart.

So okay, not a terrific investment but maybe a pretty good one? Maybe but probably not. Because Mr. Harper did not say that investors tripled their money, only that their capital had been tripled, and Blackstone gets paid substantial fees from its investors’ capital, meaning that said investors probably did substantially worse than 9.6% a year. Moreover, given the number of real-estate forward stocks, those of homebuilders and car dealerships for example, that currently yield more than 9.6% and pay a dividend, I wonder if the Motel 6 deal was more about Blackstone than its investors. Just saying!

So the meaning is this: If a deal consummated in 2012—when asset prices were far lower and competition for deals was far lower and interest rates were nearly half what they are now—underperformed the market, then what can private equity investors expect to earn nowadays? This is a question of huge concern not only to individual investors and family offices but to pension funds, which increasingly drive our economy and which have shown an increased affinity for private equity offerings, which are increasingly leveraged to boot. In other words, the Motel 6 deal is a microcosm of systemic risk.

Context makes it even more foreboding.

The earnings calls that I read each week continue to explicate a common theme: the end of economic growth in the face of exploding debt. Last week’s canary was FedEx, the huge logistic company, whose sales and profits are both falling—except in one business: its Asian exports division. Worth noting that a contingent of administration officials are in Beijing as I write this, and in the name of curbing Asian exports, because of a manufactured (pun intended) existential threat to Western culture known as Chinese “overcapacity.” Although the media discusses the overcapacity threat* as though it is established economic fact, I did not know that there was such a thing in economics or any other discipline. (At least they did not teach it at Wharton in the 1990s.)

On the contrary, what has long been assumed and taught is that, in a free market economy, supply and demand constantly fluctuate until they reach a temporary equilibrium, generally through the pricing mechanism.

But no longer! Now the free market is just a brand to be managed by price and output controls, not by Communists mind you, but by the leaders of free market economies. In other words, increasing demand—and by extension, increasing economic growth—is only desirable if the supply aspect is not Chinese. Which is a tough row to hoe, as my grandmother used to say, considering that China remains the world’s factory and that most young Westerners woudl rather be on YouTube than an assembly line.

In this context, consider the markets’ reaction to the Fed’s historic rate cut announcement on Wednesday. While the Hang Seng (Hong Kong) and the Nikkei (Japan) have gained 3.4% and 3.7% since then, respectively, the S&P 500 is up less than one percent and the FTSE (UK) is down. Indeed, the only major US index that did not fall in the hours after Chairman Powell’s speech was the small-cap Russell 2000. It took a global rally Wednesday night to prime the American markets, whose rally had petered out by Friday. Maybe investors are worrying that the markets are already flying too high, or maybe ongoing American political dysfunction, which once again threatens a governmental shutdown, is dampening optimism stateside. Or maybe Asian stock markets just look better, a little more free-markety, by comparison? I’m not clairvoyant so anything’s possible.

And this week I’ve pivoted to the Australia Securities Exchange, whose components tend to pay generous dividends and be in sound financial condition. They are rarely globally relevant, but who cares? Historically, companies of smaller size and higher quality tend to do the best, over time, whether they are on the bleeding edge of some new technology or not. Also, Australians are free thinky, adventuresome folk who don’t mind getting their hands dirty. And their major trading partner is Southeast Asia, which happens to be growing faster than any other region on earth.

True, the conventional wisdom is that bigger is better—in companies as most other things. I’ve yet to see proof (Graham disproved this theory decades ago as it pertained to big versus medium-sized stocks) yet I would never argue that size and familiarity don’t matter. Only the intelligent investor quantifies something as emotionally fraught as risk. But to leave home, the investor must set their emotions aside and calculate that the currency risk is outweighed by the political and financial risks. Given that the dollar remains at historically high levels, while faith in the government is historically low, and that neither presidential candidate seems willing to acknowledge the ballooning national debt, I’d say that this is a good bet. Terrific, actually.

James

INVESTABLES

Our index of 152 wallflowers and cigar butts has gained 7.2 percent since July 1st, excluding dividends, while the S&P 500 has gained 4.4 percent over the same time period. The index’s annualized rate of return, including most dividends, is approximately 38 percent so far this quarter. (The full index is available to paid subscribers in Excel format, upon request.)

TOP 25 LISTS:

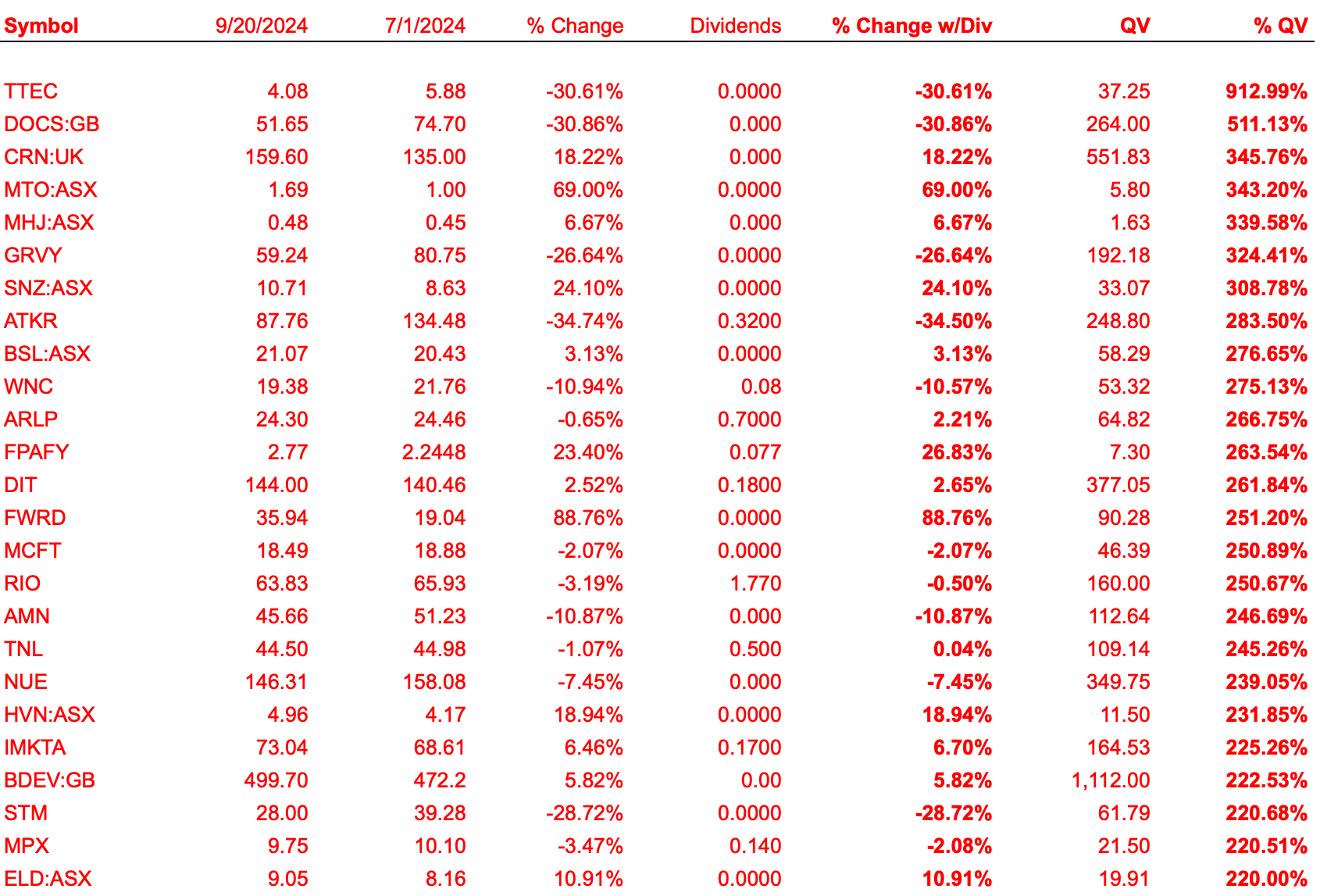

I. The Cheapstakes (based on Quantitative Value (QV) as a percentage of Friday’s closing price):

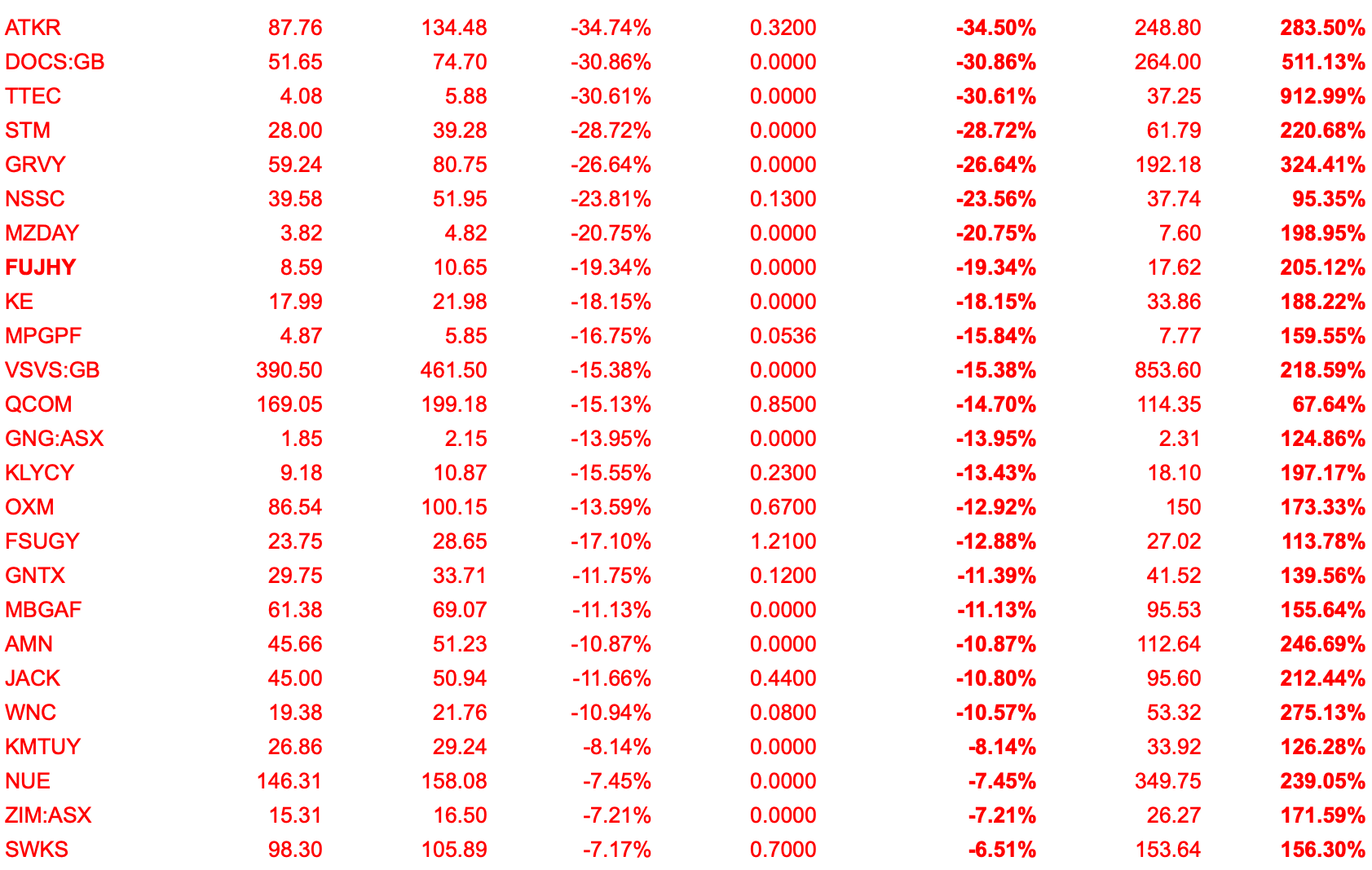

II. The Biggest Losers (based on percentage change in price since July 1st, i.e. the beginning of the rotation:

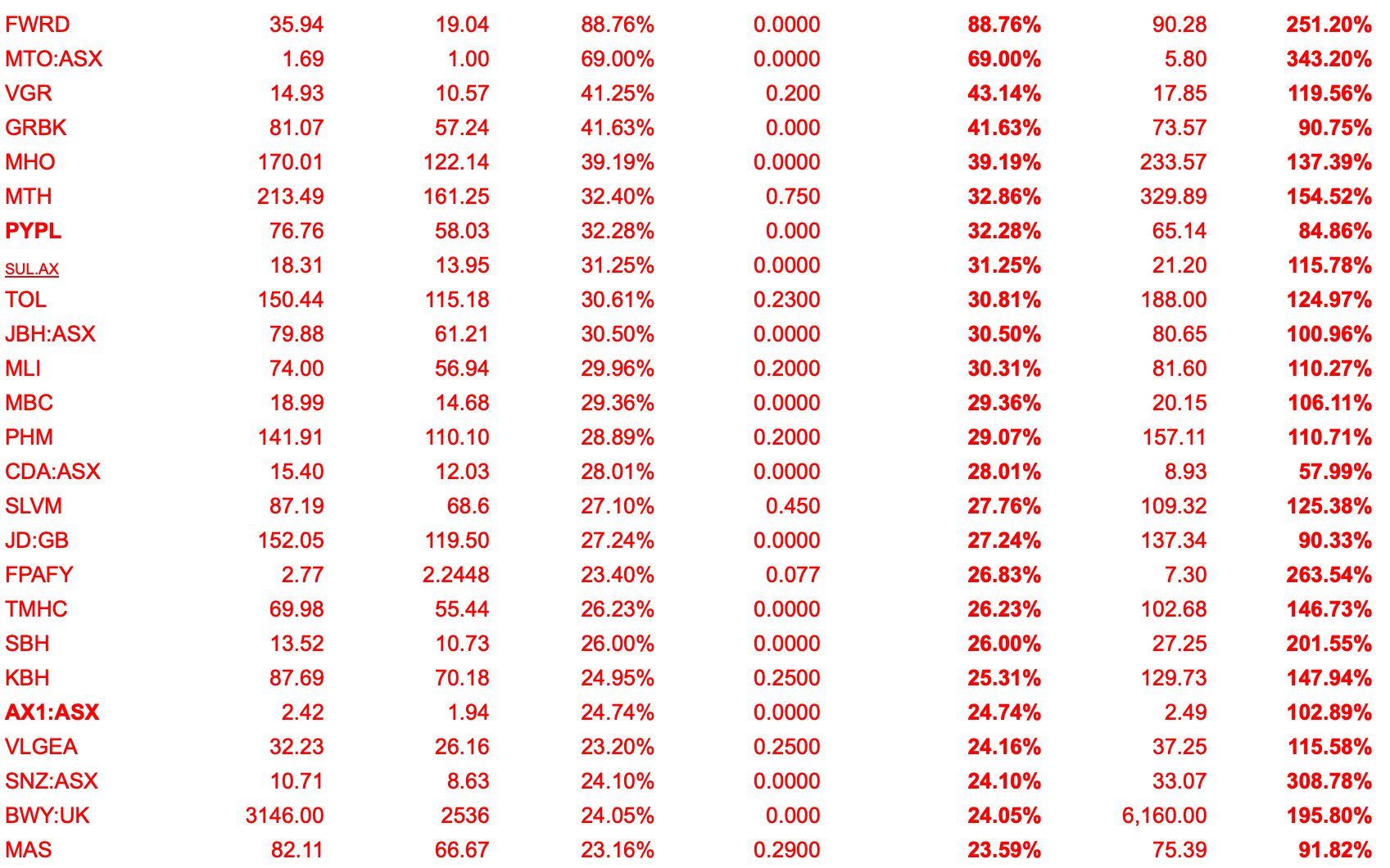

III. The Momentums (also based on percentage change in price since July 1st, i.e. the beginning of the rotation):

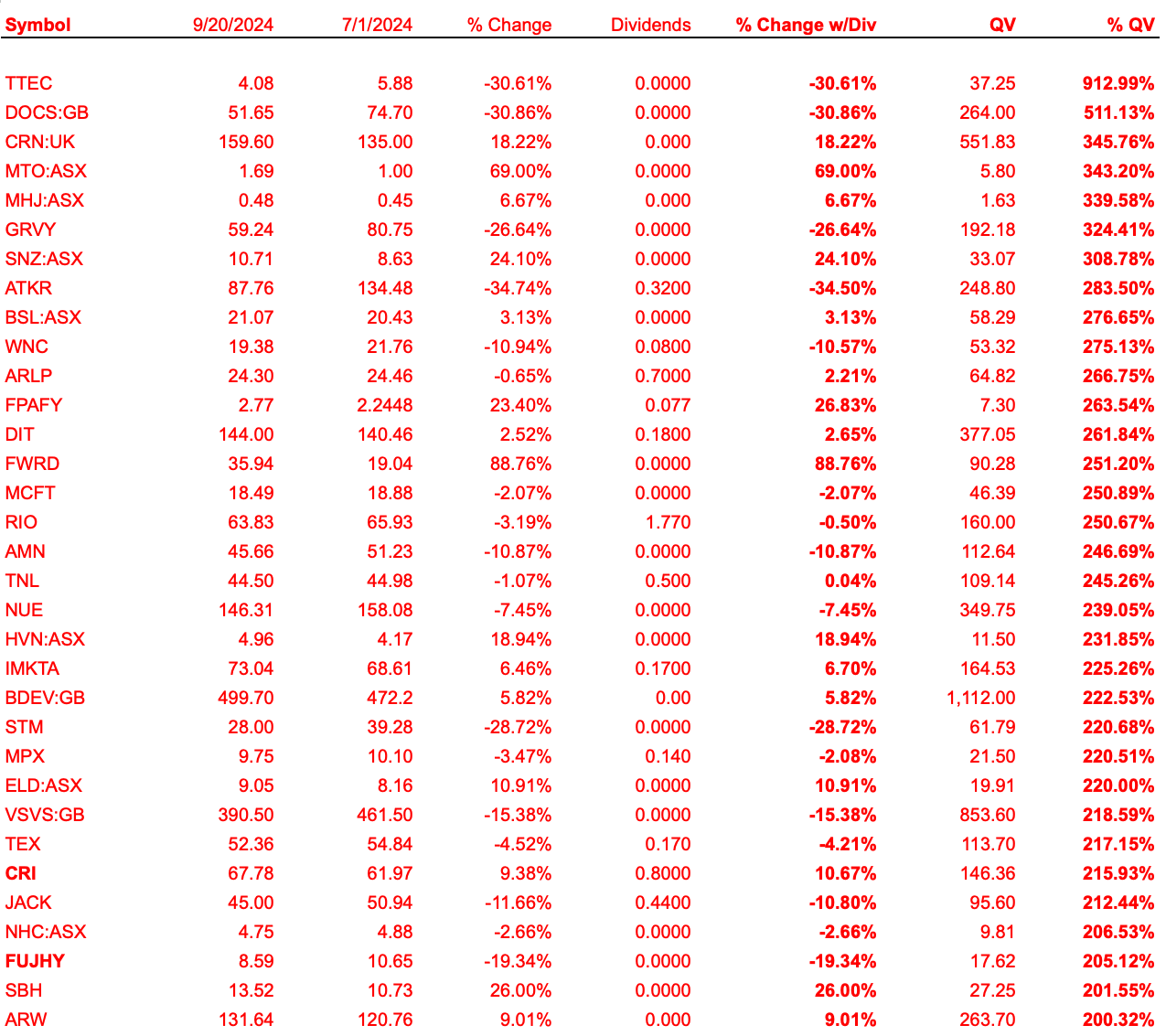

* UK and GB denote issues listed on the London Stock Exchange. ASX denotes an issue listed on the Australian Stock Exchange. All others are listed on the New York Stock Exchange or the NASDAQ.

THE 200% CLUB: Stocks whose quantitive value are at least twice (200% of) their market price as of Friday’s close:

“Fresh” Cigar Butt, culled from the Australia Securities Exchange (ASX):

GenusPlus Group Ltd. (GNP:AU)

Australian infrastructure services group.

Free cash flow (FCF) Yield: 7.4%

Dividend Yield: 1.09%

52-Weeklings

There are no cigar butts and/or wallflowers among the sixteen US-listed companies trading at 52-week lows this weekend.

WARNING: GRAPHIC CONTENT!

this is the end.