Slow Money, vol. 74

Subscriber,

Editor’s note: Last Sunday I observed that the most underpriced issue in our investables index, TTEC, was probably a bargain. Since then, TTEC shares are up 44%. - James

The rotation out of giant tech stocks took a break last week, with both the benchmark and our index kind of flat. The S&P 500 rose +0.2%; our index of investables lost -0.5%, mostly because of a correction in domestic homebuilder stocks as mortgage rates rose—either because of a rosy jobs report or because future rate cuts have been “baked in” for quite some time or both. In any event, our wallflowers and cigar butts have gained 8.5 percent since July 1st, including most dividends, while the S&P 500 has gained 5.2 percent over the same time period. Our index’s annualized rate of return, including most dividends, is therefore 38.3 percent in its first full quarter since the rotation began.

It’s Sunday morning here in Florida, and a storm is coming, so here’s a sermon:

Investing is a study in contradictions, which is what makes intelligence (or intellect, if you prefer) vital. Investing is as opposed to trading, where you just have to place the correct bet over and over again. Great traders have great instincts; great investors have great patience as well as an extraordinary ability to tolerate opposing ideas. According to Graham, the ultimate contradiction is that every investment has a speculative element; after all, even the most conservative investors speculate that the past will continue, to some extent. But the ultimate dilemma is whether or not markets are efficient. Or not.

Here Buffett and his major protege Warren Buffett, are in complete agreement and unequivocal. Because were it not for market inefficiencies, the indexes could not move up and down every moment, stocks could not gain or lose, say, 20% or more of their value in less than a day, and we could not have situations where entire stock markets go up by a third within a couple of weeks (China lately). And yet, there are a lot of very smart people who argue that markets are efficient. They too have their proof in that the vast majority of traders who test the market’s efficiency fail pretty miserably.

So which is it? Efficient or inefficient? In other words, do we or don’t we have a chance of beating market returns and creating extraordinary wealth by applying some methodology that is more rational than the market en toto? The only answer to this conundrum must be that markets become efficient by being inefficient. Put another way, markets become passive by being active. As Graham once observed, Wall Street professionals underperform the market not because they are all stupid but because they are all so smart. Their narratives cancel one another out, proving a Charlie Munger maxim: what is not worth doing is still not worth doing well.

By ignoring Munger’s wisdom, they create inefficiencies. Not because they’re dumb but because the exercise itself is stupid. For example, trying to divine the future growth rate of a company growing at 100%, or the future earnings of a company that’s never made a dime.

Enter Walter Schloss (above) Graham’s lesser protege, who understood the efficiency conundrum from ground level, and who thus trusted Graham’s method absolutely, maybe because he lacked a university education and maybe also because, like Graham, his family fortune had been destroyed in a market crash. Schloss’ partnership achieved the same returns as Graham and Buffett: twenty-one percent annually. Schloss was Wall Street’s Sherlock Holmes; he believed that knowledge, or at least short-term memory, is finite. To make the logical deduction, one must keep the attic clean, refusing to process what others are inducting, or at least not storing their speculations, especially when they’re presented as fact or conventional wisdom. Intellectually, Schloss would be followed by George Soros, founder of the most successful hedge fund in history, who boasted of his own short memory. (Soros had a world-class education but by the time he was a kid his family had lost everything to the madness of another crowd: the Nazis.) Investment success being inversely related to memory may seem counterintuitive, and memory is not the same as data by the way, but as Gore Vidal once observed, Those who can remember the past are still condemned to repeat it. Wall Street analysts put so much stock in narratives and “insights” and “color” but for information to become knowledge it must be internalized and the noise-cancelling headphones must be applied, right? No wonder Holmes wore those ear flaps!

With this in mind, my goal for the quarter is to learn something every day. We’ll see. A Hollywood acquaintance tells me that all the stories have been told, you just have to find new ways to tell them, and maybe the same is true of lessons, they just get recycled and replayed, and any computer can spot patterns. Which is the essence of macro investing, which consistently underperforms all other strategies, which is illogical but makes sense as long as everyone is doing it.

Warren Buffett says, You can’t teach a new dog old tricks. Old tricks like discounting future cash flows and adding a yield premium or margin of safety get thrown out the window when growth stocks and/or speculative fevers like AI drive the market. We have been coming out of such a time since this summer. Thankfully, just as you can make new TV and film with old stories, so too can investors make money new money from old companies, and old companies can make money from old consumers, who have most of the money by the way. They will have to, since the economy is no longer growing much, and hot air does not create economic tailwinds as it does hurricanes.

Yet there’s still a lot of non-growth companies trading at growth prices, even within the so-called Magnificent 7. Many of these are former growth companies with legacy valuations. Others have been non-growth companies for a long time, but they’ve used financial engineering and non-GAAP accounting to juice their earnings per share, and thus their share price. When interest rates were near zero, this was a great party trick: borrow free money, buy back shares and increase EPS; repeat. Which is how a profitable company like Apple ended up with over one hundred billion dollars of debt on its balance sheet. But the effectiveness of financial engineering is inversely related to interest rates. It’s also subject to the law of diminishing marginal utility. At some point, financial engineering actually shifts earnings into reverse because the interest payments reduce earnings that are not being juiced by buying back shares with “free” money.

So the pendulum has swung and companies are adjusting on the fly. Techs are abandoning their moon shots and trimming the fat while spending on the new moon shot: AI. Financial engineering now means cutting existing expenses—i.e. expenses associated with existing businesses— while capitalizing new ones. This may work as well as the old strategy, then again it may not. Many investors and even some analysts pay a lot of attention to cash flow, and 50/50 is not investing odds. This leaves the intelligent investor with few options.

The option of the moment is to invest in growth economies, for example China, India and Southeast Asia generally. For this to sustain, currencies must remain pretty stable and regulation must be pretty transparent. Also, the urban Chinese middle class must not slouch back to the abject poverty of the farm and/or rice paddy.

Another option is to invest in financial assets, for example real estate and crypto and private loans, in the hope that their prices can continue to grow faster than the underlying economies themselves. In this case, real interest rates must fall, as lower interest rates are the only reliable way to increase the value of financial assets.

Finally, one can invest in non-giant companies that have long runways of double digit growth, say one or two decades’ long. Over time, though not recently, this has proved the best way to achieve outsized returns—in other words, beating the market by not being the market.

Since I don’t give advice here, I’ll quote a popular song instead: Good Luck Babe!

Indexes

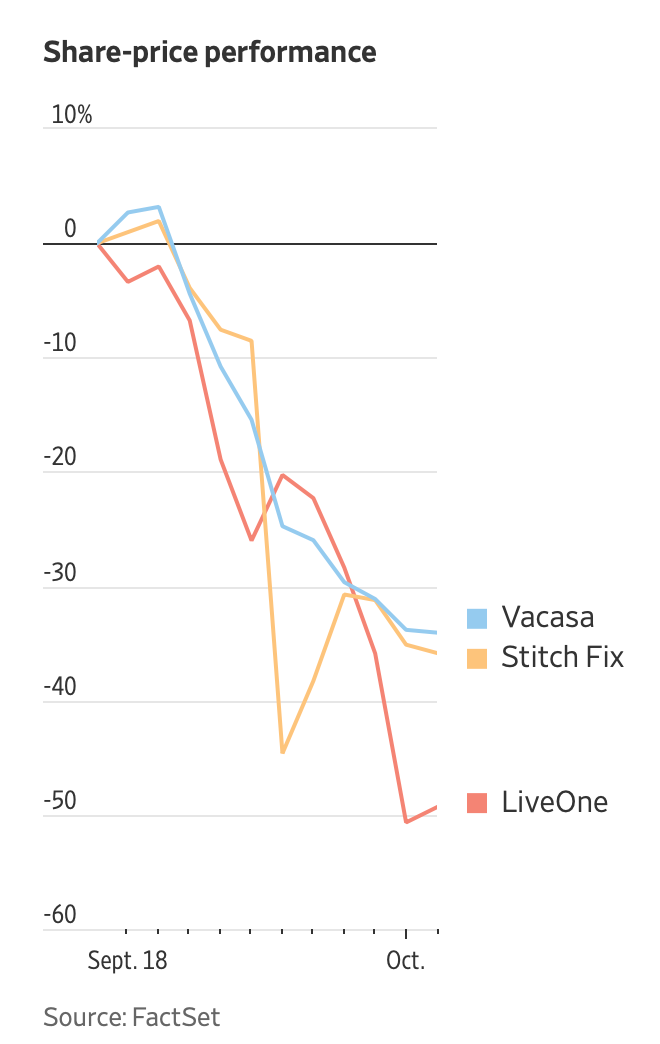

On Thursday, The Wall Street Journal published this article titled, “If a Soft Landing is in the Cards, Why Aren’t Small-Cap Stocks Rallying after the Fed’s Interest-Rate Cut?” Which seems to contradict what I’ve been writing since July. Except that the article’s question is dumb and the author’s answer is even dumber. The former because two weeks (the time since said interest rate cut) is meaningless, particularly when the cut was anticipated for months, over which time small-cap stocks have indeed outperformed; the latter is misleading because, as noted here, we would not expect small-stocks to rally en toto but rather we would see interest shifting to profitable small stocks, and particularly those with a yield premium. Which is what’s happening (see first paragraph). So there.

When I quoted Oracle’s CEO’s cautionary take on the media a couple of weeks ago, I was referring to exactly this type of article. By cherry-picking some dates and using an index that is (literally) full of crap, the Journal may be literally correct. But God the acrobatics! The three small stocks that the author chose (see graph above) in order to justify their headline are all zombies, i.e. none is profitable. Moreover, LiveOne trades for pennies while Stitch Fix and Vacasa are essentially never-weres, meaning that they are ideas that have yet to prove themselves as businesses—and may not. Are we to be surprised that a half-point Federal Reserve rate cut has not solved flawed business models? Of course not. And even The Journal knows better.

Because a couple of months ago it ran an article titled, “The Junk in Your Index Fund Is Costing You Big-Time.” This was specifically about all the zombies like LiveOne, Stitch Fix and Vacasa (click here) in popular ETFs and indexes like (you guessed it!) the Russell 2000. Just as we are learning that achieving lasting peace is not a passive exercise, so too achieving sustainable returns, even if countless ads on the Journal’s website say otherwise.

At least Wall Street’s paper of record still publishes a list of issues trading at their 52-week lows, which was Walter Schloss’ favorite section. Go figure.

James

INVESTABLES

TOP 25 LISTS:

Editor’s Note: These will be the three subindexes used to track the relative performance of the strategies going forward. - James

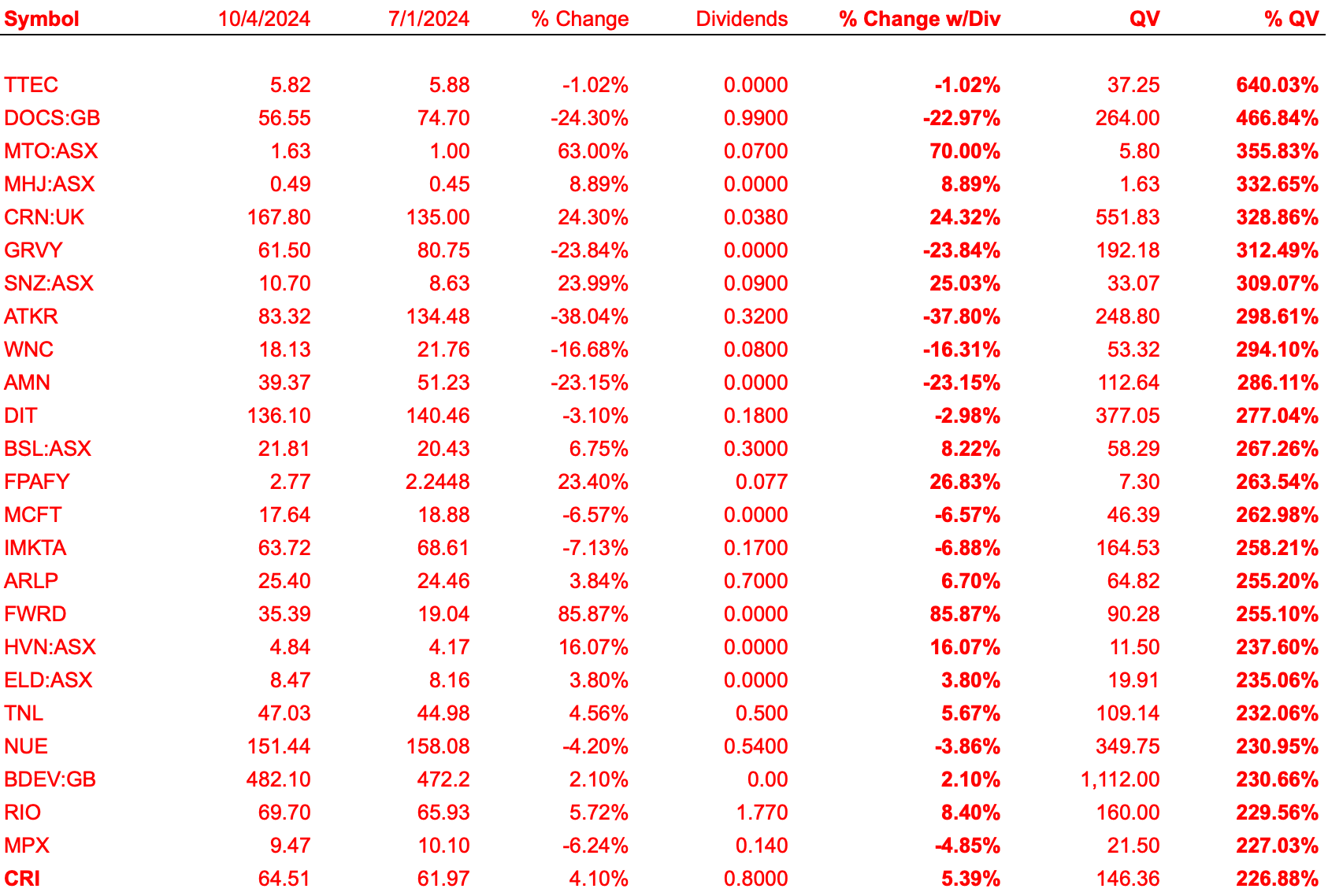

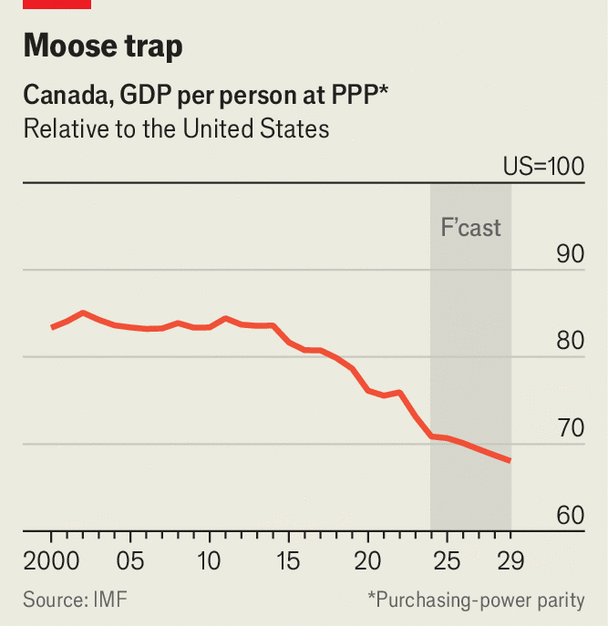

I. The Cheapstakes (based on Quantitative Value (QV) as a percentage of Friday’s closing price):

II. The Biggest Losers (based on percentage change in price since July 1st, i.e. the beginning of the rotation:

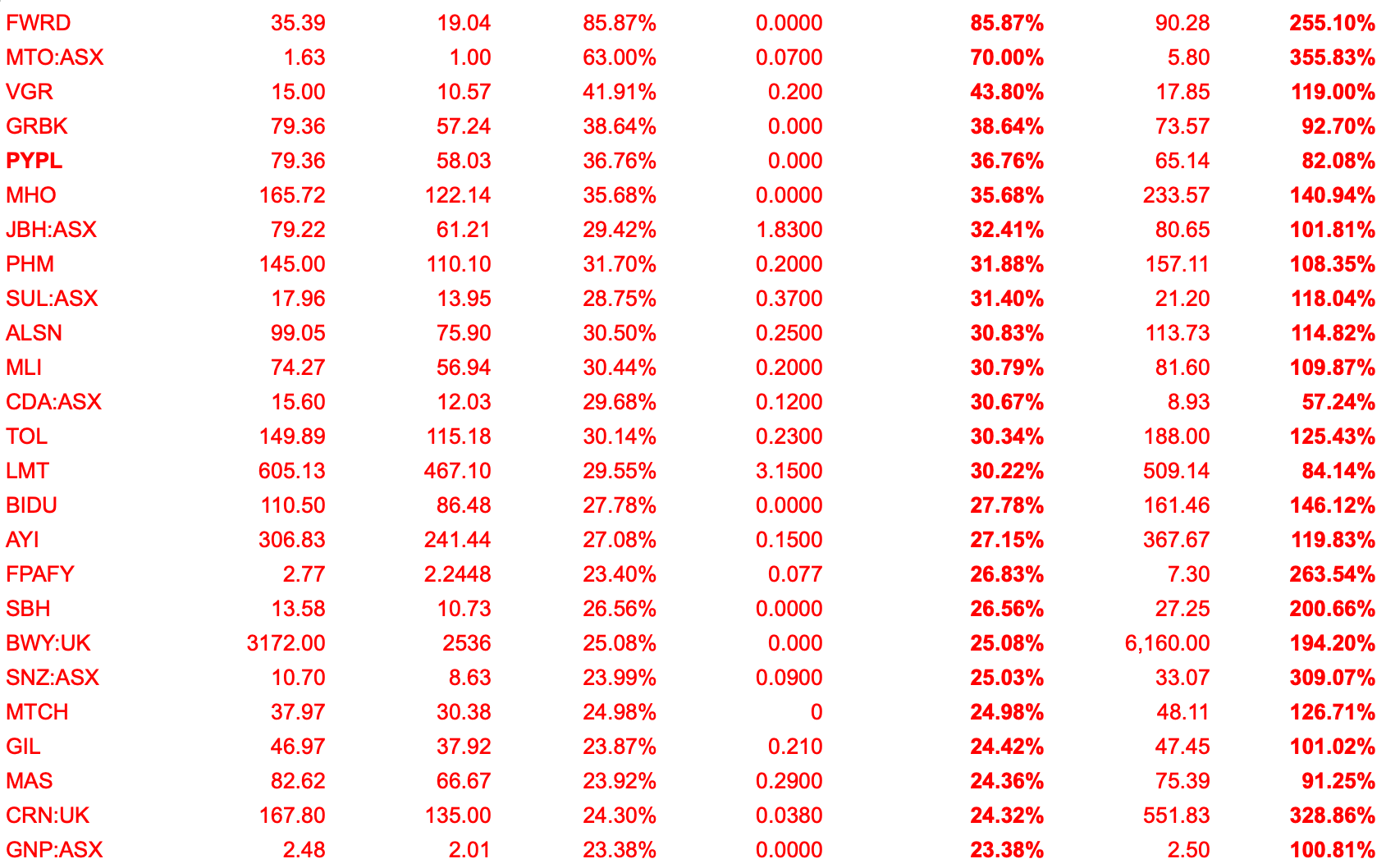

III. The Momentums (also based on percentage change in price since July 1st, i.e. the beginning of the rotation):

* UK and GB denote issues listed on the London Stock Exchange. ASX denotes an issue listed on the Australian Stock Exchange. All others are listed on the New York Stock Exchange or the NASDAQ.

THE 200% CLUB: Stocks whose quantitive value are at least twice (200% of) their market price as of Friday’s close:

There are no “fresh” cigar butts or wallflowers this week.

52-Weeklings

Cigar butts and/or wallflowers among the fifteen US-listed companies trading at 52-week lows this weekend:

AMN Healthcare Services Inc (AMN)

Healthcare staffing.

Free cash flow (FCF) Yield: 24.4%

Dividend Yield: -

WARNING: GRAPHIC CONTENT!

this is the end.