the receipts issue

Subscriber,

Since its inception on October 20th, 2020, our rolling portfolio has achieved a 28% average annual return. Which is extraordinary, but also unbelievable for some. Ergo this “receipts” issue, in which every portfolio iteration is published below, along with summary information.

Why now? Selfishly I’d like to sell more paid subscriptions, advisory services and classes. There is also the matter of pride in an experiment that has done (and continues to do) splendidly, despite many mistakes. So I hope that you’ll take a moment to scan the data below, keeping in mind the following:

These returns are extraordinary but not that surprising. Warren Buffett, Walter Schloss and Ben Graham himself all achieved 21% annual returns through decades. Indeed, over the same time period as our portfolio, Berkshire Hathaway (BRK.B) has returned 21.6% annually, while shares of Buffett disciple Bill Ackman’s Pershing Square have returned 18.7% annually. This versus 14% and 11.7% for the S&P 500 and S&P 600 respectively. As for momentum traders, Cathie Woods’ flagship ETF (ARKK) has lost more than half of its value over the same time period.

It’s really not about the stocks. If you are skeptical of these returns, you will most likely not internalize their lesson but here goes anyway: the Graham approach is not stock-picking; it is risk management. The stocks below are not bets; rather, they are components of carefully curated risk pools.

Finally, a challenge. In lieu of an audit (I have triple-checked the numbers myself, but bias and all that) I invite any reader, and there are hundreds, including many finance professionals, to check these results against past newsletters and publicly available data. If your results are meaningully different than mine, I’ll publish them promptly and give you a refund.

James

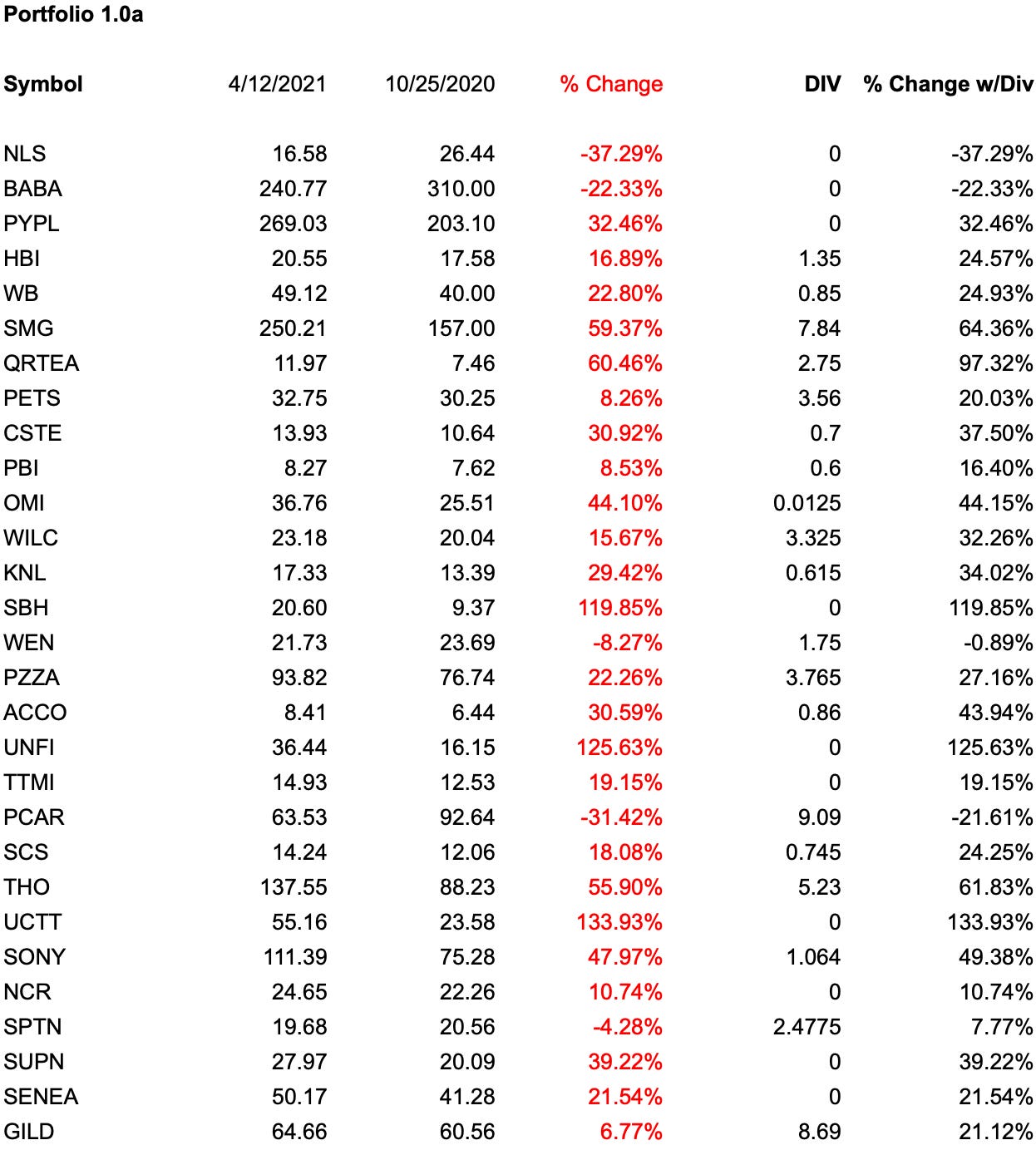

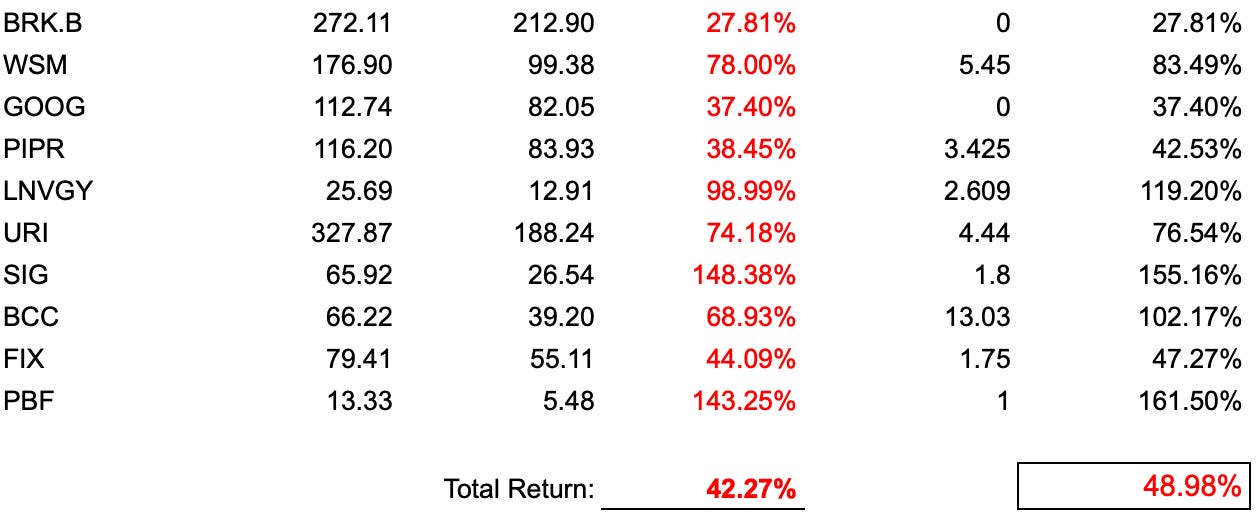

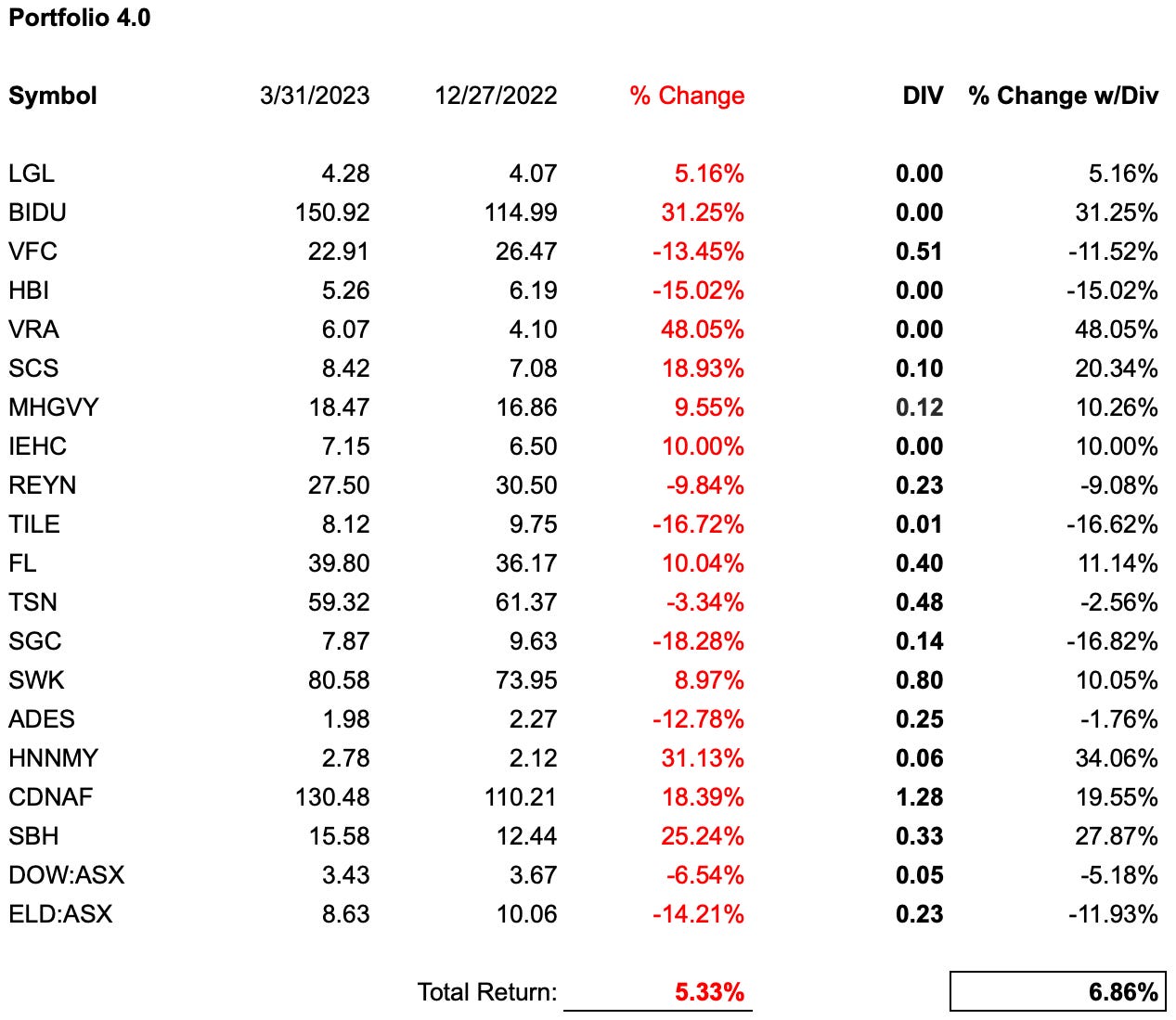

Ed. Note: The first date is the portfolio end date, and the numbers below that are the prices at market close. The second date is the portfolio start date, and the numbers below that are the average of the day’s high and low price. The only exception is the Roaring Twenty, whose component end prices are as of Saturday morning and therefore may be slightly different from Friday’s close in some cases. All portfolios were announced at least one day in advance of tabulations; the same goes for their closing dates. Colors are for internal purposes and have no meaning.